Treasury Yield Curve Steepens. Bond Marketplace a Wee Bit Anxious?

By means of Wolf Richter for WOLF STREET.

Treasury yields and the now un-inverted and properly steepening Treasury yield curve handed any other landmark on Friday, perhaps the primary such landmark ever: Whilst the Fed minimize its coverage charges by means of a complete share level, long-term yields have risen by means of a complete share level.

Since September 16, the low level two days prior to the speed minimize, the 5-year yield has risen by means of 106 foundation issues, the 7-year yield by means of 105 foundation issues, the 10-year yield by means of 100 foundation issues, and the common 30-year mounted loan price by means of 100 foundation issues.

The ten-year Treasury yield reached 4.62% on Friday, the easiest since Might 1 (pink), whilst the Efficient Federal Budget Price (EFFR), which the Fed goals with its coverage charges, used to be 4.33% (blue). This equivalent transfer into reverse instructions of the EFFR and the 10-year yield is fantastic.

The yield curve steepened properly after un-inverting fully.

With longer-term Treasury yields emerging, whilst non permanent Treasury yields haven’t modified a lot right through the week – not pricing in any price cuts right through their time window – the yield curve has steepened additional, after it un-inverted fully every week in the past.

On the longer finish, 5-year and 7-year yields rose by means of 8 foundation issues right through the week, whilst 10-year and 30-year yields rose by means of 10 foundation issues, with the 30-year yield emerging to 4.82%, the easiest since April.

The chart beneath displays the yield curve of Treasury yields around the adulthood spectrum, from 1 month to 30 years, on 3 key dates:

Gold: July 25, 2024, prior to the hard work marketplace information spiraled down (which used to be a false alarm).

Blue: September 16, 2024, the low level two days prior to the Fed’s preliminary minimize.

Purple: Friday, December 27, 2024.

Even supposing the yield curve has gently steepened this week, it stays quite flat, with just a 31-basis level unfold between the 2-year yield (4.31%) and the 10-year yield (4.62%), however that unfold has widened from 22 foundation issues every week in the past.

In different phrases, traders are accepting nonetheless low time period premiums. But if the yield curve used to be inverted till not too long ago, longer-term yields have been less than non permanent yields and the time period top rate used to be damaging.

Because the yield curve normalizes, it’s going to steepen additional and time period premiums will upward thrust. This might occur in two techniques: With shorter-term yields falling or with long-term yields emerging, or each.

Why the divergence of the 10-year yield from the EFFR?

Some of the number one causes the Fed minimize its coverage charges by means of 100 foundation issues, because it identified again and again, have been the loosening hard work marketplace stipulations and the considerable cooling of inflation since mid-2022.

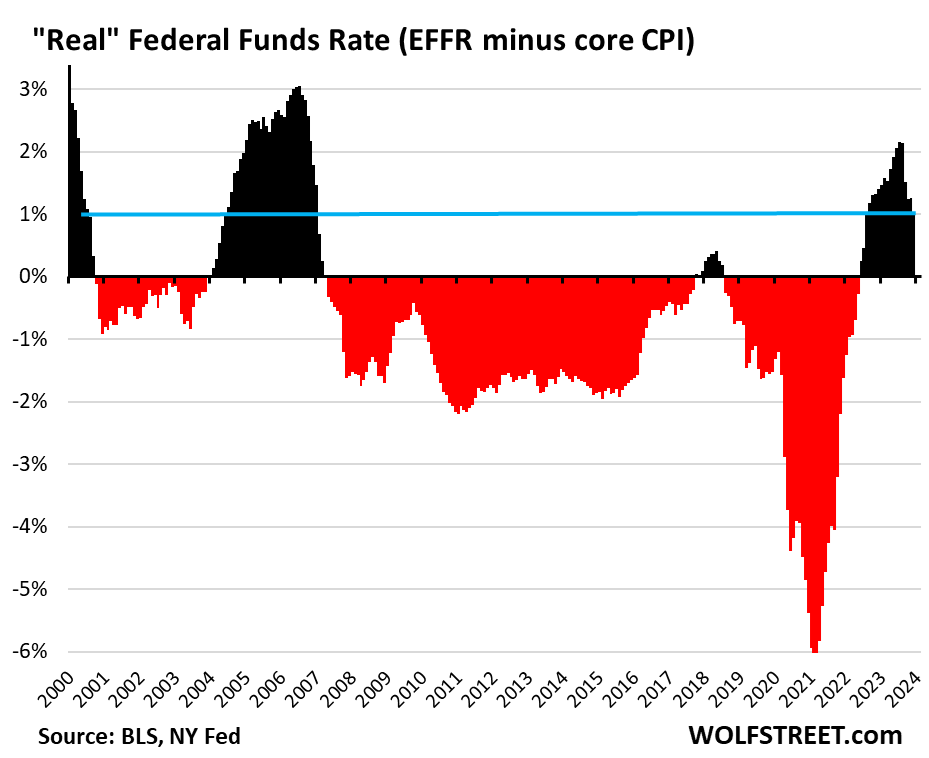

The hard work marketplace stays somewhat cast, however it shouldn’t loosen additional, the Fed mentioned. And inflation has cooled from the highs in 2022, with all primary inflation charges – CPI (2.7%), core CPI (3.3%), PCE value index (2.4%), and core PCE value index (2.8%) – smartly beneath the Fed’s coverage charges and smartly beneath the EFFR (5.33% prior to the cuts, 4.33% lately).

With inflation charges less than the EFFR, the “actual” EFFR is sure (adjusted for inflation). In comparison to November core CPI, the easiest of the primary inflation readings at 3.3%, the true EFFR lately is +1.0%. Since 2008, the true EFFR used to be most commonly damaging.

However the Fed didn’t minimize as it noticed a recession coming. Seeing a recession is the traditional explanation why for reducing charges, however the financial system has been rising at a tempo this is considerably upper than the 15-year common, there is not any recession in sight, and financial enlargement turns out to have picked up in the second one part, operating above 3%.

The truth that the Fed has hiked charges so rapid and thus far, and has stored them there for goodbye, and that inflation has cooled such a lot, with out the financial system going right into a tailspin, however cruising alongside at an above common tempo, is traditionally bizarre.

Quicker financial enlargement continuously ends up in upper longer-term yields. Conversely, recessions result in low longer-term yields. Most often when the Fed begins reducing charges, it sees a recession, and longer-term yields are falling together with the Fed’s coverage charges for the reason that bond marketplace too is seeing that recession.

However this time round, the Fed minimize amid above-average financial enlargement and not using a recession in sight – in order that’s bizarre – and longer-term yields have risen amid this cast financial enlargement.

The bond marketplace is getting a wee bit fearful.

Inflation considerations are actually re-emerging. It’s been warming up once more in contemporary months. The Fed itself on the final assembly projected a state of affairs of upper inflation by means of the top of 2025 than now, and better “longer-run” coverage charges, and its diminished its projections for price cuts from 4 to simply two in 2025 for the ones causes. Powell on the press convention mentioned that the speed minimize were a “shut name,” and doubts emerged right through the click convention that there can even be two cuts subsequent yr.

And there are considerations that persisted stimulative fiscal insurance policies and further price lists will supply additional gas for inflation.

As well as, there are emerging considerations within the bond marketplace concerning the ballooning US debt, and concerning the flood of recent provide of Treasury securities that the federal government should promote in an effort to fund the out-of-whack deficits. Treasury consumers and holders are unfold in every single place, however upper yields could also be important to reel within the mass of recent consumers wanted, even because the Fed is losing its Treasury holdings via QT.

Those are worrisome ideas for doable consumers of long-term Treasury securities; they need to be compensated via upper yields for the dangers of upper inflation and the dangers this flood of recent provide would possibly deliver.

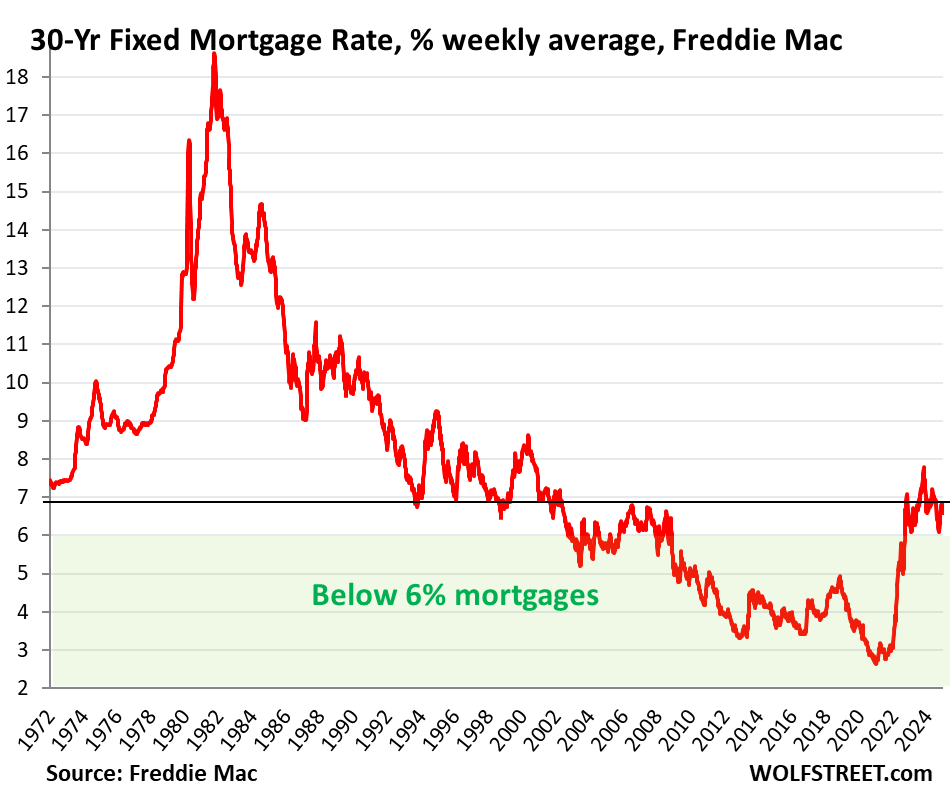

Loan charges again round 7%.

For the reason that price minimize in September, the common 30-year mounted loan price has risen by means of 100 foundation issues, from 6.11% to 7.11% on Friday, in keeping with the day-to-day measure from Loan Information Day by day.

The weekly measure from Freddie Mac has risen by means of 77 foundation issues over this era, to six.85%. Those upper loan charges in spite of 100 foundation issues in price cuts have pushed the true property trade up the wall.

However the ones 6%-plus mortgages have been commonplace within the a long time prior to 2008, even right through occasions of price cuts. It’s simplest after 2008, when the Fed’s QE and interest-rate repression distorted the whole lot, that those low-rate mortgages started to reduce to rubble the housing marketplace. So perhaps it’s time to get re-used to some of these loan charges that have been commonplace prior to 2008.

Experience studying WOLF STREET and need to make stronger it? You’ll be able to donate. I respect it immensely. Click on at the beer and iced-tea mug to learn the way:

Do you want to be notified by way of e mail when WOLF STREET publishes a brand new article? Enroll right here.

![]()

")