quite a lot of communicate the 10-year yield will revisit 5%, which is humorous only a few months after Price-Reduce Mania.

Through Wolf Richter for WOLF STREET.

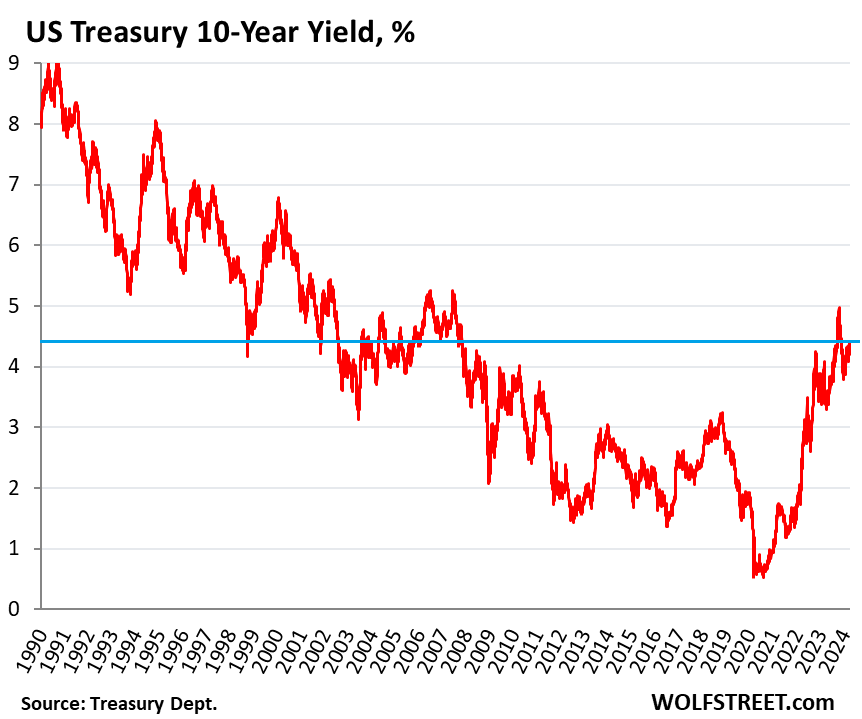

The ten-year Treasury yield rose to 4.40% on Friday, the absolute best since November 27. All over rate-cut mania in December, the yield had dropped underneath 3.80%.

The ones strikes in fresh days and weeks added up, they usually level to a steady reputation within the bond marketplace that inflation charges might be upper than what they’d been prior to the pandemic, that 2% inflation isn’t going to occur, and that the super-low interest-rate setting during the last 15 years – culminating in August 2020 when the 10-year yield used to be all the way down to 0.5% – is over.

What comes subsequent is unknown, but it surely’ll most probably entail upper inflation of the kind observed within the Nineties and prior to since the Fed isn’t keen to crash the economic system and the exertions marketplace simply to get to two% inflation.

That implies the Fed will stay its coverage charges quite prime – prime sufficient not to let inflation spiral out of keep watch over, however no longer so prime as to crash the economic system and produce inflation down to two% – and yields might be upper too to make amends for the upper inflation, the whole lot might be upper, adore it was once, and the bond marketplace is adjusting to that state of affairs.

Now there’s unexpectedly quite a lot of communicate that the 10-year yield will revisit 5%, the place it had in brief been in October, as a result of inflation might be upper for longer, or without end, which is humorous after Price-Reduce Mania, and the yield must make amends for inflation over the 10-year length, plus some.

Clearly, “without end” right here doesn’t imply without end within the cosmic sense, however within the bond sense, which means past the adulthood date of the bond.

It’s attention-grabbing how the narrative available in the market modified so briefly. From November into mid-January, there used to be the Price-Reduce Mania, with the marketplace for federal price range futures seeing very prime possibilities of 5 and 6 fee cuts or even seven fee cuts in 2024, unfold over the 8 Fed conferences.

After which the Fed began pushing again. It got here out with a doozie of a push-back FOMC observation after its January assembly, and repeated it at its March assembly. And we had two terrible inflation readings in January and February, on best of the upward pattern of the underlying metrics that began closing fall.

The “dot plot” from the March FOMC assembly confirmed that the nineteen members had been just about flippantly break up, with 9 seeing two fee cuts in 2024, and 9 seeing 3 fee cuts, and 1 seeing 4 cuts, leaving the median at 3 cuts. But when simplest probably the most three-cutters turns into a two-cutter via the June dot plot, then a two-cuts state of affairs comes out of that assembly. This March “dot plot” used to be a serious warning call that the ones 3 fee cuts might vanish.

Since then, quite a lot of Fed officers gave speeches, fretting concerning the trail of inflation, and strolling again their very own rate-cut expectancies.

The day past, Minneapolis Fed President Kashkari mentioned the quiet section out loud: Possibly there received’t be any fee cuts in 2024 if inflation assists in keeping going “sideways.”

These days Fed governor Bowman got here out and mentioned out loud: “Whilst it isn’t my baseline outlook, I proceed to peer the danger that at a long run assembly we might want to build up the coverage fee additional must development on inflation stall and even opposite.”

They’re speaking about non permanent coverage charges, no longer longer-term yields. And so they’re fretting that one thing large has modified within the economic system: That even the 5.25% to five.5% non permanent coverage charges, that had been intended to be “restrictive” and that had been broadly anticipated to throw the economic system right into a recession, have no longer been restrictive and feature no longer slowed the economic system.

To the contrary, financial enlargement and the exertions marketplace speeded up in 2023, and the exertions marketplace has maintained its fast enlargement thus far in 2024, growing jobs at a fee of three.3 million a yr within the first quarter, which is sizzling, and warmer than it used to be in 2023. And fiscal prerequisites have eased, and markets are in la-la-land.

And so other people are questioning what sort of coverage fee would if truth be told be “restrictive” if 5.5% on the present inflation charges isn’t restrictive. If inflation on a three-month foundation and six-month foundation is 4% or 5%, the place would coverage charges must be to be restrictive?

The 3-month core CPI speeded up to 4.2% annualized, the absolute best since Would possibly 2023, and the three-month core products and services CPI speeded up to five.6%.

Coverage charges are 5.25% to five.50%. They want to be upper than inflation charges to be restrictive; there may be well-liked settlement on that. Simply how a lot upper is unsure.

There are numerous inflation measures in the United States. But when we use the three-month measure of core CPI, which used to be 4.2% in February, impartial coverage charges may well be 6.0%, and the rest underneath would nonetheless be stimulative.

Clearly, everybody is simply guessing. Inflation has come down so much, however now it’s heading upper once more. The trail of inflation may be very unsure, as we have now observed. It would flip round and move down once more, however that turns out not likely now. Inflation often dishes out head-fakes.

The economic system and the exertions marketplace had been rising at an above-average tempo, and but coverage charges had been above 5% since Would possibly 2023 and above 4% since December 2022. With that more or less enlargement, and the inflation we have now, they’re no longer restrictive.

And the bond marketplace is adjusting to this state of affairs and it sort of feels is simply heading again to the outdated standard – the standard from 20 or 30 years in the past, as we will be able to see within the long-term chart:

Revel in studying WOLF STREET and wish to toughen it? You’ll be able to donate. I respect it immensely. Click on at the beer and iced-tea mug to learn the way:

Do you want to be notified by way of electronic mail when WOLF STREET publishes a brand new article? Join right here.

![]()