Fed shed 26.5% of Treasuries it had added all over pandemic QE.

By way of Wolf Richter for WOLF STREET.

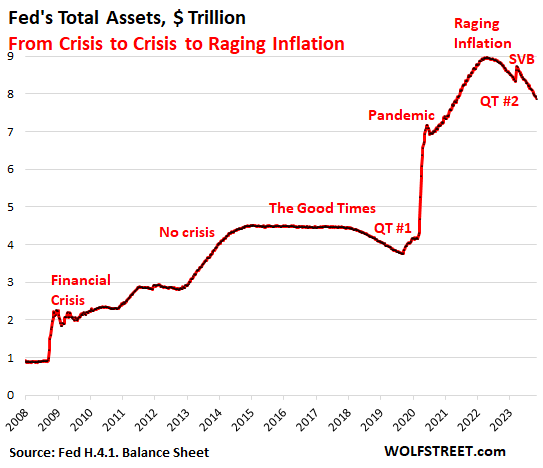

The Fed’s Quantitative Tightening (QT) and the unwinding of the bank-panic liquidity measures proceed on course: General belongings at the Fed’s stability sheet dropped through $89 billion in October, to $7.87 trillion, the bottom since Might 2021, in line with the Fed’s weekly stability sheet nowadays.

Since peak-QE in April 2022, general belongings have dropped through $1.10 trillion. The close-up view:

From disaster to disaster to raging inflation:

All the way through this $1.1 trillion drop in belongings beneath QT #2, inflation has sponsored off from its rage in 2022, nevertheless it’s nonetheless just about two times the Fed’s goal.

In contrast, all over QT #1 between November 2017 and August 2019, when the Fed’s general belongings dropped through $688 billion, inflation was once underneath or on the Fed’s goal (1.8% core PCE in August 2019), and the Fed was once simply looking to “normalize” its stability sheet.

However now there’s numerous inflation nonetheless, and the QE asset-pile ballooned when the Fed went hog-wild all over the pandemic, and now there’s much more to take off the pile. The lengthy view:

QT on course.

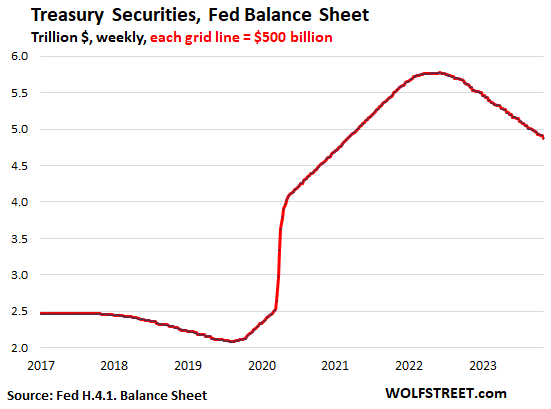

Treasury securities: -$58 billion in October, -$899 billion from height in June 2022, to $4.87 trillion, the bottom since March 2021.

The Fed has shed 27.5% of the $3.27 trillion in Treasury securities it had piled on all over pandemic-QE.

Treasury notes (2- to 10-year securities) and bonds (20- & 30-year securities) “roll off” the stability sheet mid-month or on the finish of the month once they mature and the Fed will get paid face price for them. The roll-off is capped at $60 billion per 30 days, and about that a lot has been rolling off, minus the inflation coverage the Fed earns on Treasury Inflation Secure Securities (TIPS) which is added to the essential of the TIPS.

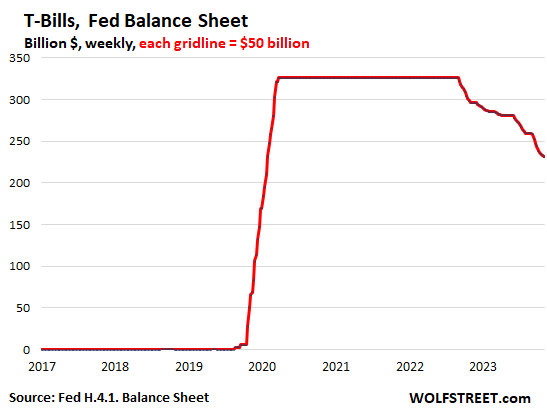

Why Treasury payments are vital for QT. Those non permanent securities (1 month to at least one yr) are incorporated within the general Treasury securities of $4.87 trillion at the Fed’s stability sheet.

They display us when the roll-off of notes and bonds falls in need of the $60-billion per thirty days cap, as a result of T-bills are then used to make up the adaptation. And when the Fed runs out of T-bills, the Treasury roll-off will fall underneath the $60 billion cap.

There have been handiest 3 months this yr – February, Might, and August – when the roll-off of notes and bonds exceeded the $60 billion per thirty days cap, so the roll-off was once capped at $60 billion.

Within the different seven months this yr, the roll-off of notes and bonds was once underneath the cap, and T-bills had been used to make up the adaptation. In October, $7 billion of T-bills had been used for this objective.

From March 2020 throughout the ramp-up of QT, the Fed held $326 billion in T-bills that it continuously changed as they matured through purchasing new T-bills at auctions. That is evidenced through the flat line within the chart underneath.

In September 2022, T-bills first began rolling off as had to best off the Treasury roll offs.

At the present stability sheet, T-bills are all the way down to $231 billion, with the opposite $95 billion in T-bills having through now been used to best off the Treasury roll-off.

The stash of T-bills at the stability sheet tells us that the Fed will hit the $60 billion cap every month. As soon as that stash is long gone, the roll-off of Treasuries will then most commonly now not succeed in the $60 billion cap.

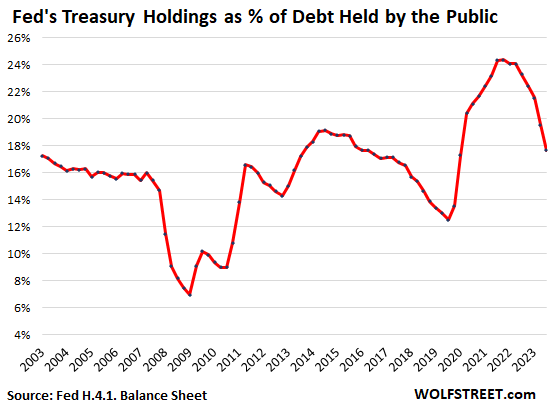

The Fed’s weight within the Treasury marketplace: The Fed now holds 17.7% of marketable Treasury securities held through the general public, down from over 24% on the height. The pointy drop within the share is a results of two components: One, the QT drop in Treasury securities at the Fed’s stability sheet; and two, the ballooning marketable securities issued to fund the large deficit.

In different phrases, the Fed nonetheless performs a large function within the bond marketplace, however that function is hastily declining in relative phrases:

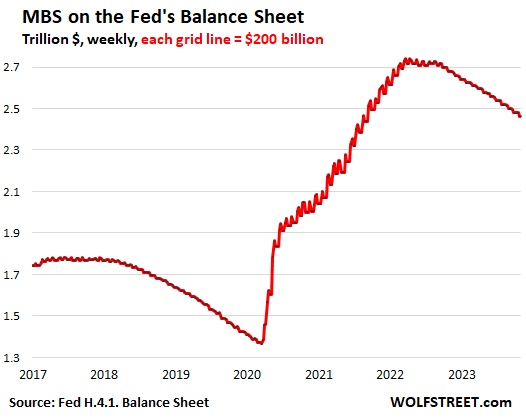

Loan-Subsidized Securities: -$17 billion in October, -$277 billion from the height, to $2.46 trillion, the bottom since September 2021.

The Fed handiest holds government-backed MBS, and taxpayers lift the credit score possibility. MBS come off the stability sheet essentially by the use of pass-through essential bills that holders obtain when mortgages are paid off (mortgaged properties are bought, mortgages are refinanced) and when loan bills are made.

The spike in loan charges has brought about refis to cave in and residential gross sales to plunge which slowed the loan payoffs, and due to this fact the pass-through essential bills, with the MBS run-off between $15 billion and $21 billion a month, a ways underneath the $35-billion cap.

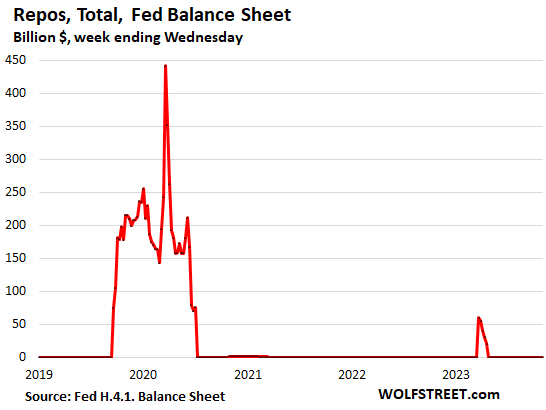

Financial institution-panic liquidity pile unwinds.

Repos are available in two flavors, each $0 now. Repos with “overseas legitimate” counterparties – most probably the Swiss Nationwide Financial institution in its efforts to backstop the take-under of Credit score Suisse through UBS – had been paid off in April. On the height in March 2023, they reached $60 billion.

The traditional repos with US counterparties pale out in July 2020, when the Fed made the phrases much less horny. The Fed these days fees 5.5% on repos, as a part of its coverage charges, which it left unchanged the day gone by, and there are not any takers at those charges. However there have been numerous takers all over the disaster in March via June 2020, and when the repo marketplace blew out in overdue 2019. That’s the large bulge within the chart underneath.

The little bulge in early 2023 had been the repos with overseas legitimate counterparties.

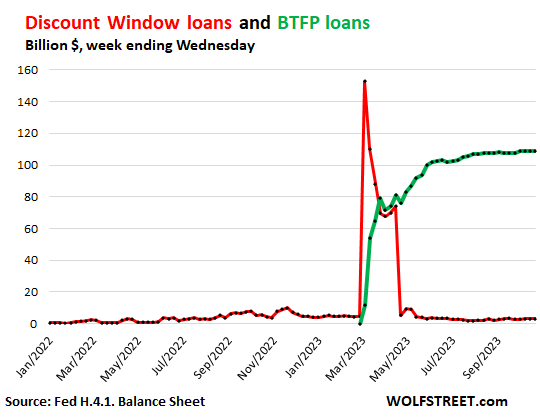

Bargain Window: more or less unchanged in October, on the near-nothing stage of $2.9 billion, in comparison to $153 billion in bank-panic March (crimson line within the chart underneath).

Bargain Window lending to banks is as outdated because the Fed. The Fed these days fees banks 5.5% to borrow on the cut price window, and banks need to put up collateral beneath strict stipulations and at “truthful marketplace price.” Banks repay those pricey Bargain Window loans once they are able to.

Financial institution Time period Investment Program (BTFP): ticked up through $1.4 billion in October to $109 billion (inexperienced line within the chart underneath).

The BTFP, created all over the financial institution panic, is much less punitive and extra versatile than the Bargain Window. Banks can borrow for as much as 365 days, at a hard and fast fee, pegged to the one-year in a single day index change fee plus 10 foundation issues. The collateral is valued at acquire value moderately than on the decrease marketplace value.

This facility is small in comparison to the $22.8 trillion in business financial institution belongings held through the 4,100 business banks in the USA.

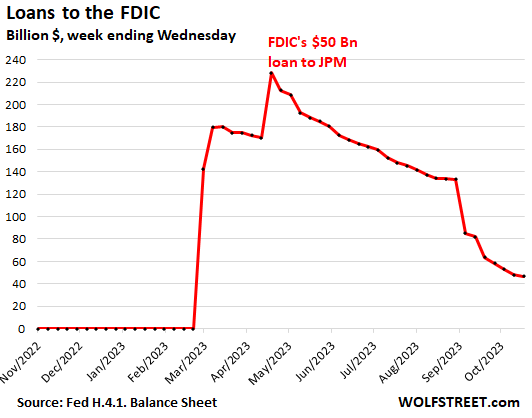

Loans to FDIC: -$16 billion in October, to $47 billion.

The FDIC has been promoting the belongings it took on with the takedowns of Silicon Valley Financial institution, Signature Financial institution, and First Republic. After the asset gross sales shut, the FDIC sends the proceeds from the gross sales to the Fed to pay down the mortgage stability. The FDIC additionally issued a $50 billion mortgage to JPMorgan to fund a part of the First Republic liabilities that JPMorgan took on.

Revel in studying WOLF STREET and wish to toughen it? You’ll be able to donate. I respect it immensely. Click on at the beer and iced-tea mug to learn how:

Do you want to be notified by the use of e-mail when WOLF STREET publishes a brand new article? Join right here.

![]()

")