Six-month core PPI: +3.4%. Six-month services and products PPI: +3.7%. Yr-over-year, each additionally speeded up additional. However power costs plunged.

By way of Wolf Richter for WOLF STREET.

The plunge in power costs brought about the Manufacturer Worth Index to inch up by way of simply 0.05% in September from August – rounded to “unchanged” – and this used to be the fabric lately for the (AI-generated?) headlines. However out of doors of power, inflation on the manufacturer stage wasn’t benign in any respect, as a number of of the prior monthly adjustments had been revised up considerably lately. The six-month averages, which come with the revisions, and the year-over-year will increase, display that the entire state of affairs modified for the more severe.

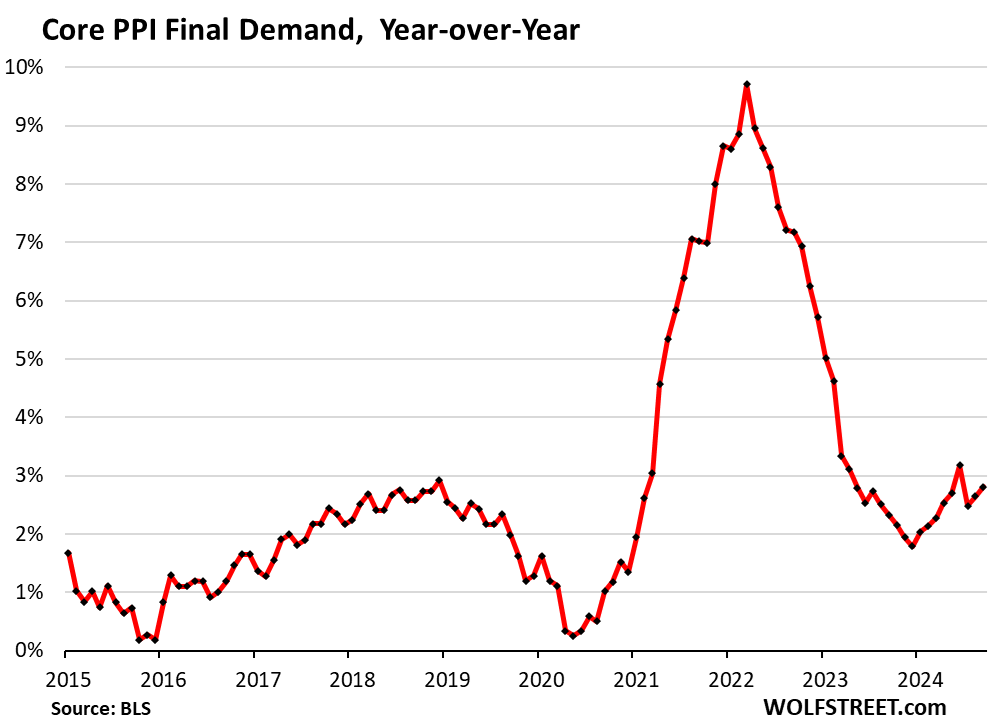

“Core” PPI rose 1.9% annualized in September from August (0.16% now not annualized), seasonally adjusted, in line with knowledge from the Bureau of Hard work Statistics lately. However probably the most prior months had been revised up considerably. Those monthly squiggles are indicated in blue.

So the 6-month Core PPI – which contains the revisions and irons out the monthly squiggles – speeded up to +3.4% in September. With regards to the up-revisions: August, as revised lately, rose by way of 3.2%, up from the August studying a month in the past of two.8%. Observe how the 6-month reasonable shifted upper in 2024, after being well-behaved in a lot of 2023 close to 2% (crimson).

Yr-over-year, core PPI rose by way of 2.8%, the second one month in a row of accelerations, appearing a vital up-trend in all of 2024. With regards to the up-revisions: August, as revised lately, rose by way of 2.6%, up from the studying a month in the past of two.4%.

The PPI tracks inflation in items and services and products that businesses purchase and whose value will increase they in the long run attempt to cross directly to their consumers.

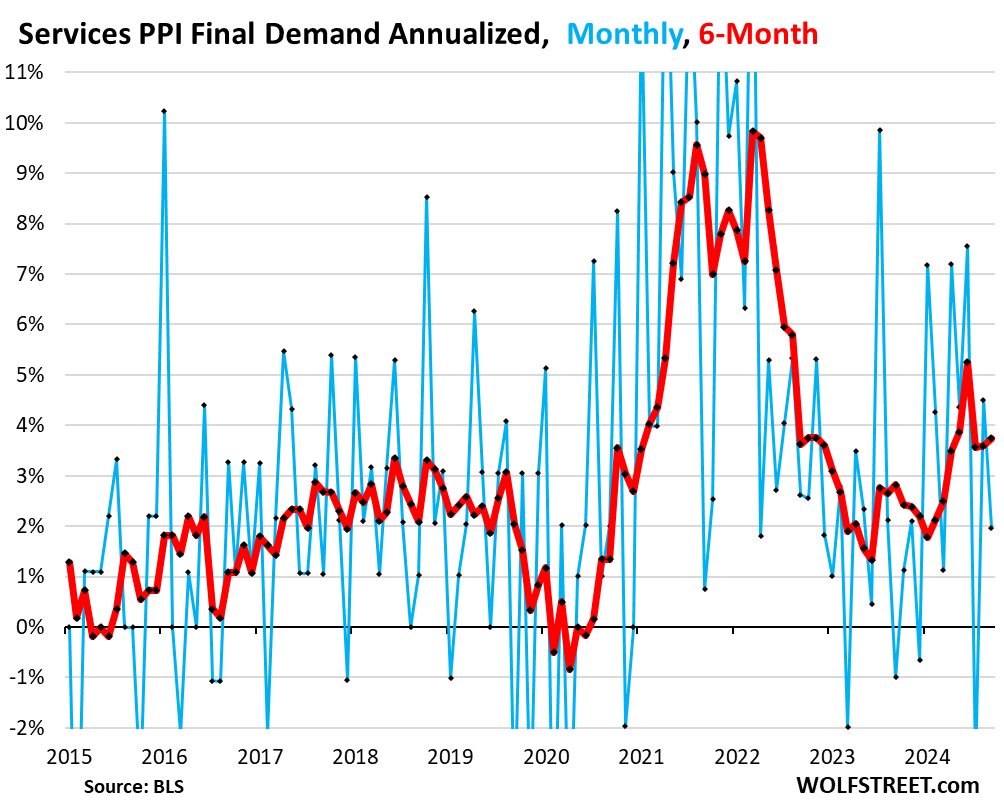

Products and services PPI rose by way of 2.0% annualized in September from August, and probably the most prior months had been revised up considerably (blue within the chart under).

So the 6-month reasonable rose by way of 3.7% (annualized) in September. With regards to the up-revisions: August, as revised lately, rose by way of 3.6%, up from the August studying a month in the past of three.0%!

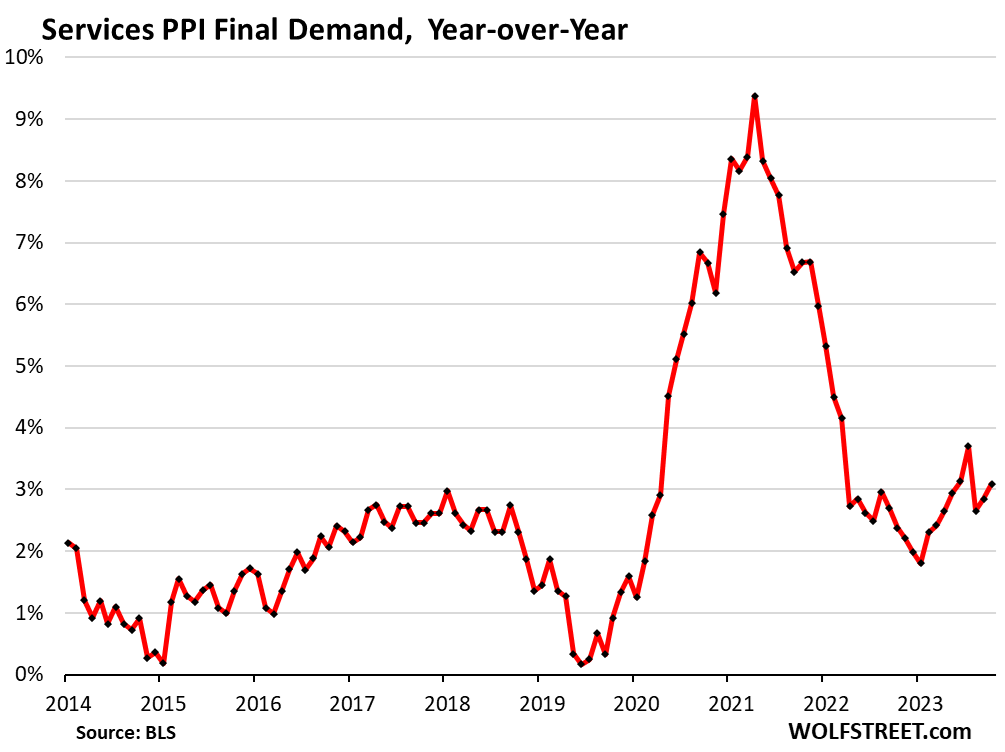

It’s the massive revisions within the services and products PPI that drove the revisions within the core PPI. And there’s not anything benign concerning the fashion within the services and products PPI.

Yr-over-year, the services and products PPI speeded up to a few.1% in September. With regards to the revisions: August used to be revised as much as an building up of two.9%, from an building up of two.6% reported a month in the past.

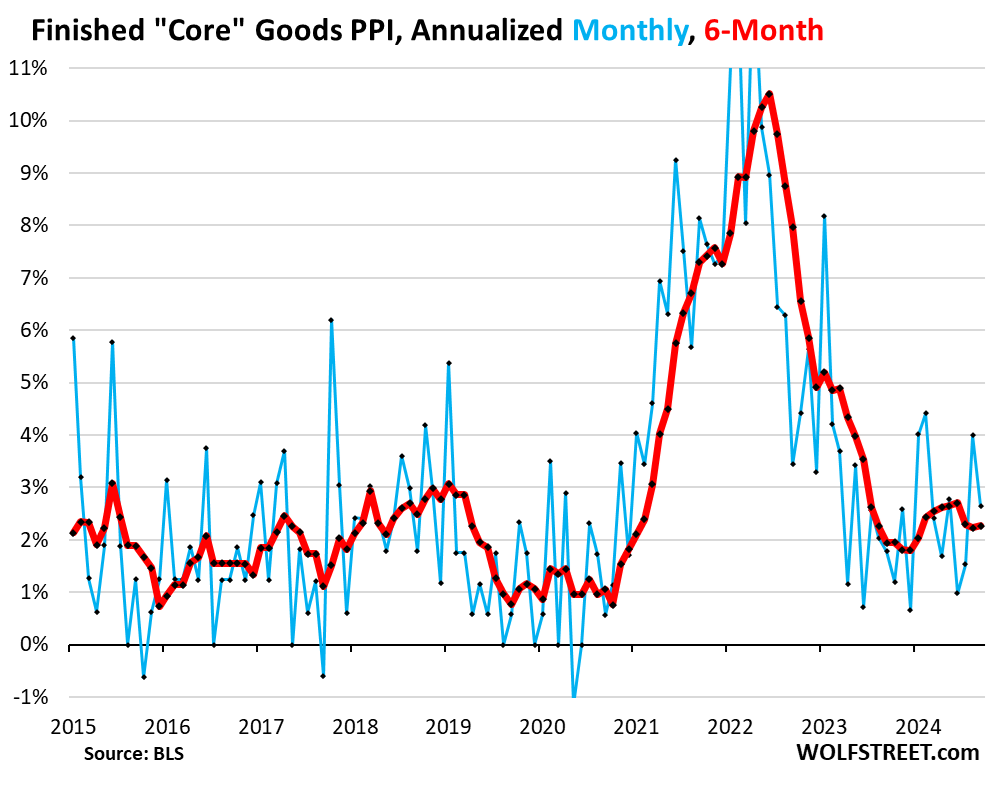

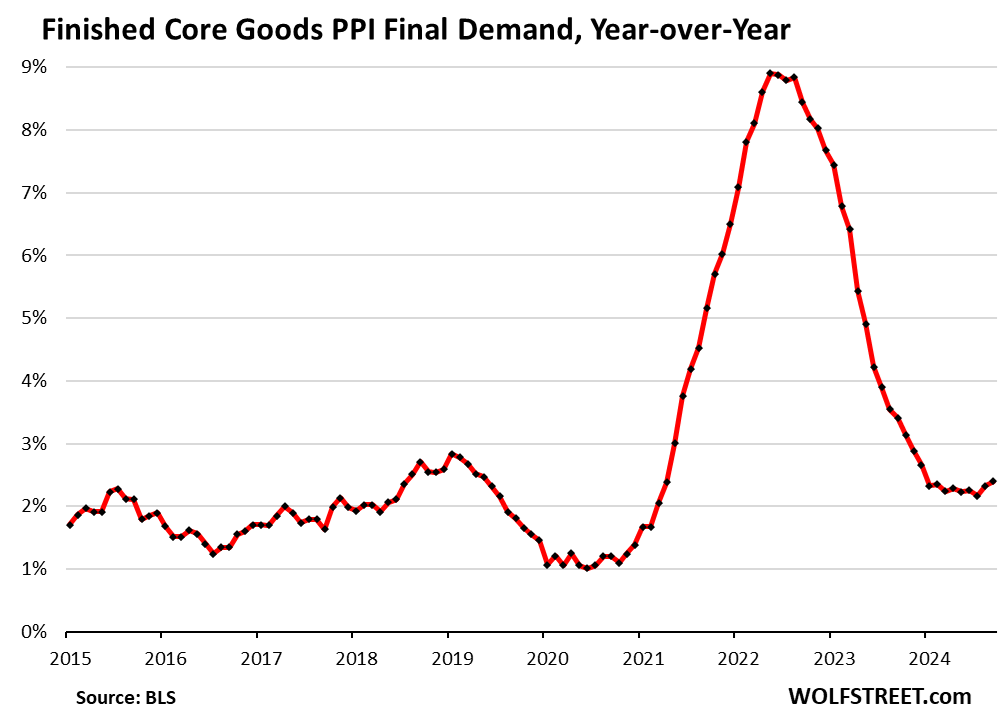

“Completed core items” PPI rose by way of 2.6% annualized in September from August. The 6-month reasonable speeded up to two.3%, however has been in that vary for 3 months. And the revisions had been insignificant.

On the core items stage, manufacturer worth inflation appears to be within the higher portion of the pre-pandemic vary at this level.

As we’ve got observed within the Shopper Worth Index as nicely, there were no primary inflation pressures in core items in over a yr. Inflation has gotten very sticky in services and products. And core items had been a large consider conserving general inflation down.

The PPI for “completed core items” contains completed items that businesses purchase however excludes meals and effort merchandise.

Yr-over-year, the completed core items PPI speeded up to two.4% in September, the perfect since December 2023. Right here too, we will be able to see that core items inflation is within the higher portion of the pre-pandemic vary.

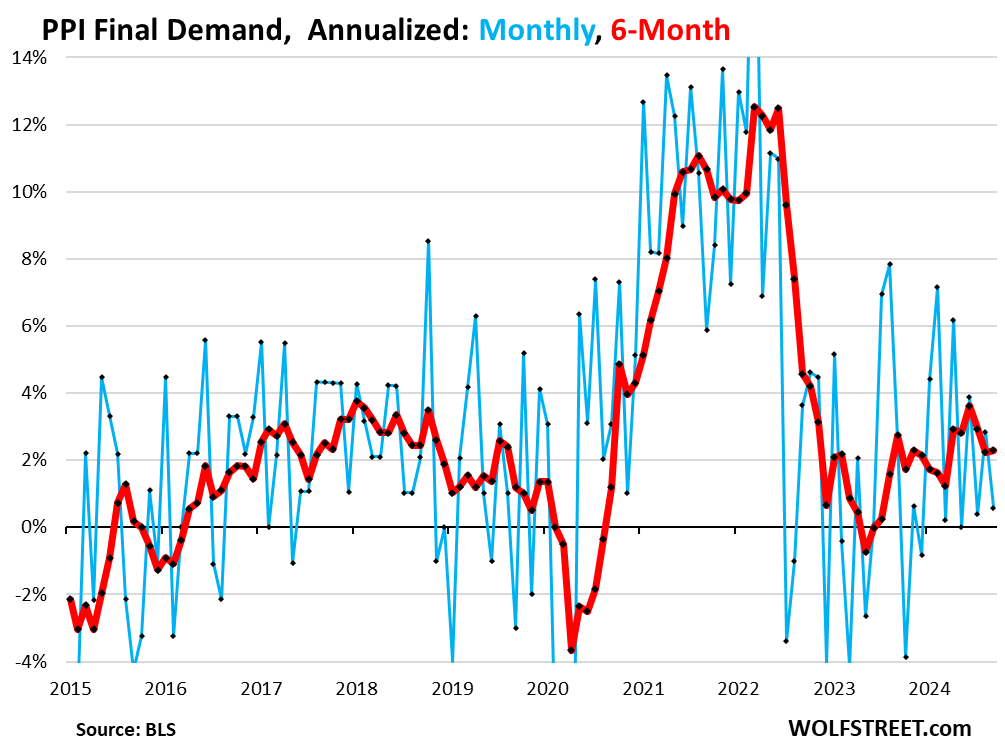

The full PPI for ultimate call for, pushed down by way of the plunge in power costs, inched up 0.6% annualized in September from August (+0.05% now not annualized).

However the large up-revisions of the prior months brought about the 6-month reasonable to boost up to an building up of two.3%, in spite of the plunge in power costs.

With regards to the revisions: August used to be revised as much as an building up of two.2%, from the rise reported a month in the past of one.9%.

Right here too, and in spite of the plunge in power costs, we will be able to see that general PPI began trending upper in 2023.

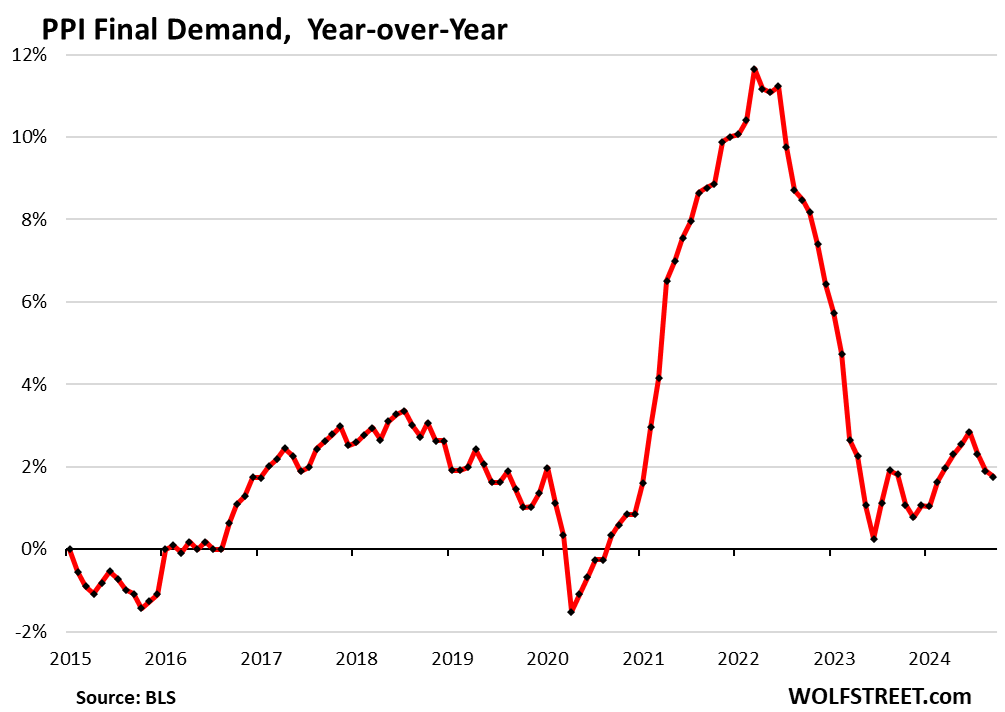

Yr-over-year, general PPI rose by way of 1.8%. The August building up used to be revised as much as 1.9%, from the 1.8% building up reported a month in the past.

Clearly, the huge plunge in power costs, which began in mid-2022, will finish when power costs hit backside someplace. Power costs can’t plunge endlessly. However this plunge in power costs has papered over the very sticky and nonetheless colourful inflation pressures in services and products, which is why we have a look at costs past power.

Experience studying WOLF STREET and need to give a boost to it? You’ll donate. I recognize it immensely. Click on at the beer and iced-tea mug to learn how:

Do you want to be notified by the use of electronic mail when WOLF STREET publishes a brand new article? Enroll right here.

![]()

:max_bytes(150000):strip_icc()/GettyImages-2190848732-e82ca8b164c74252a2f47b0e20fee915.jpg "S&P 500 Positive factors and Losses These days: Tech Shares Fall to End Vacation Week")