Costs are nonetheless manner too prime, however… “Consumers are in a greater place to barter because the marketplace shifts clear of a supplier’s marketplace”: NAR.

By means of Wolf Richter for WOLF STREET.

Pending house gross sales – a forward-looking indicator of “closed gross sales” over the following couple of months – clearly plunged in November from October on account of the Thanksgiving week, and this time they plunged via 20.1% from October, in keeping with the Nationwide Affiliation of Realtors these days. However they do this kind of factor each November, and so NAR makes use of large seasonal changes to iron out the monthly plunge, and this time grew to become it right into a monthly upward push of two.2%.

In comparison to the collapsed ranges in November ultimate yr, now not seasonally adjusted pending gross sales rose 5.6%, whilst seasonally adjusted pending gross sales rose 6.9%. July had set an rock bottom within the historical past of the knowledge.

So in comparison to the Novembers in prior years, seasonally adjusted, pending gross sales have been up from rock-bottom, however stay within the frozen zone because the Consumers’ Strike continues as a result of costs are too prime (historical information within the chart by the use of YCharts):

November 2022: +4.6%

November 2021: -33.5%

November 2020: -37.2%

November 2019: -26.9%.

Pending gross sales are in accordance with contract signings and observe offers that haven’t closed but and may just nonetheless fall aside or get canceled.

Pending gross sales via area.

Seasonally adjusted, transactions fell within the Northeast (-1.3%), inched up within the Midwest (+0.4%) and within the West (+0.5%), and jumped within the South (+5.2%).

No longer seasonally adjusted, transactions plunged in all 4 areas (-27.0%, -26.2%, -20.3%, and -12.9% respectively).

What NAR mentioned about this case:

“Customers gave the impression to have recalibrated expectancies relating to loan charges and are making the most of extra to be had stock.”

“Loan charges have averaged above 6% for the previous 24 months. Consumers are not looking ahead to or anticipating loan charges to fall considerably.”

“Moreover, patrons are in a greater place to barter because the marketplace shifts clear of a supplier’s marketplace.”

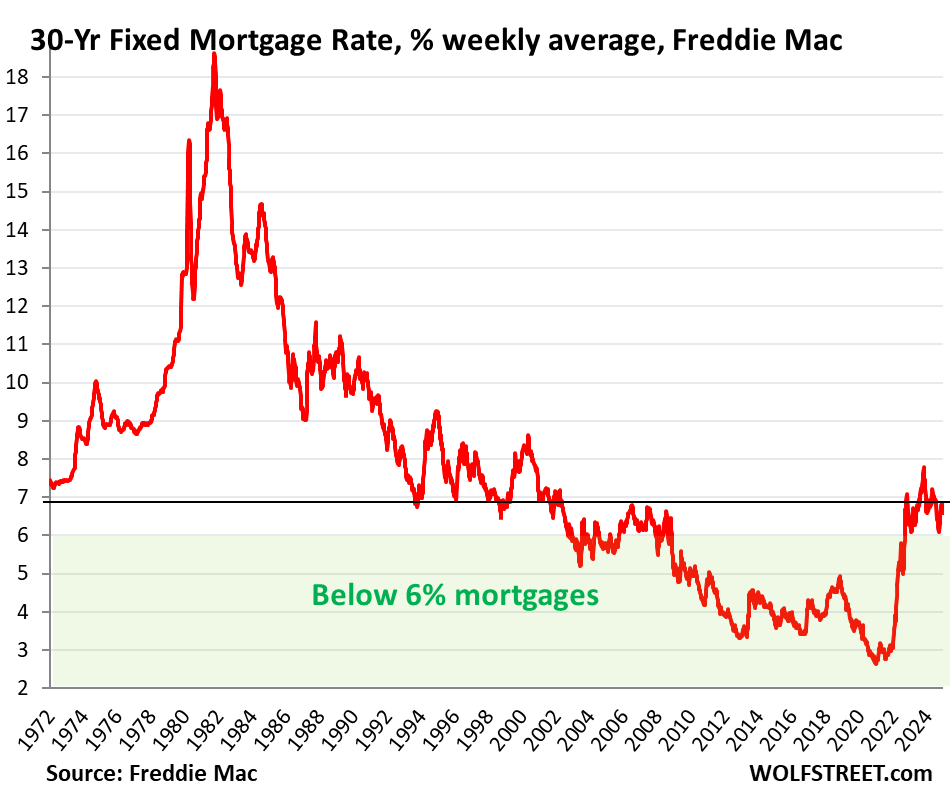

Loan charges are again within the old-normal vary.

The common 30-year mounted loan price, as of December 26, rose to six.85%, in keeping with Freddie Mac’s weakly measure.

In November, when the ones pending offers have been made, that measure of loan charges used to be nonetheless slightly decrease, within the vary between 6.69% to six.84%.

The ones charges are a ways upper than that they had been all over the Fed’s rate of interest repression and QE, which incorporated purchasing trillions of greenbacks of mortgage-backed securities. However that segment resulted in early 2022. And in mid-2022, the Fed began losing securities, together with MBS, and has thus far shed $2.1 trillion of its overall holdings.

So loan charges are actually again into the previous traditional vary sooner than QE, and the business, together with NAR and Fannie Mae, are beginning to counsel that the ones extra-fancy low loan charges aren’t coming again, and that it’s time to get re-used to the old-normal loan charges.

Provide is piling up – together with from new building.

Consumers now have a number of stock to choose between, together with closely promoted new properties (to not talk of recent condos, of which there’s a flood of provide available on the market and coming available on the market, which isn’t incorporated within the figures right here).

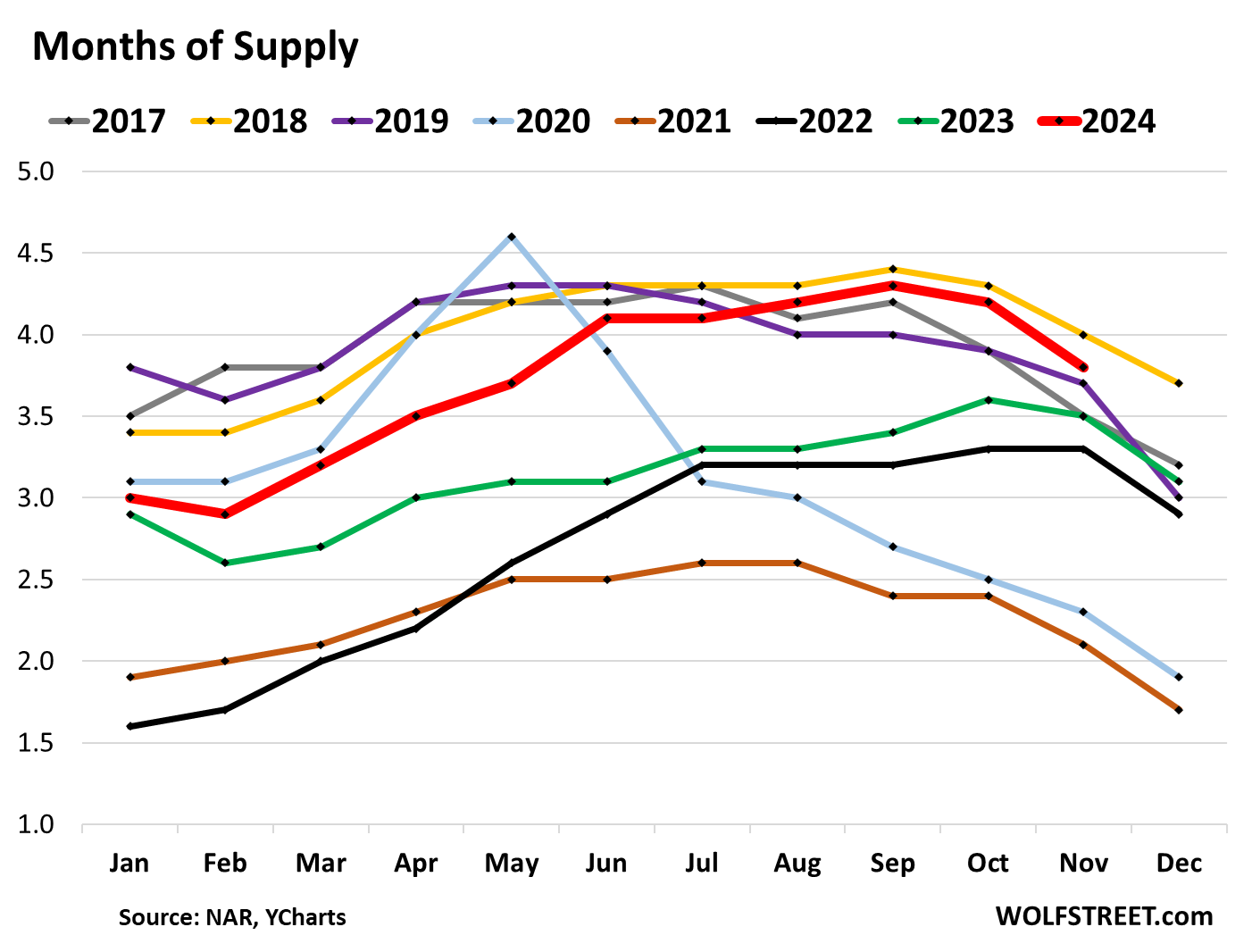

Provide of current houses on the market, at 3.8 months (pink line within the chart underneath), used to be the second one absolute best for any November over the last 8 years, 2017 thru 2024, at the back of handiest 2018 (yellow).

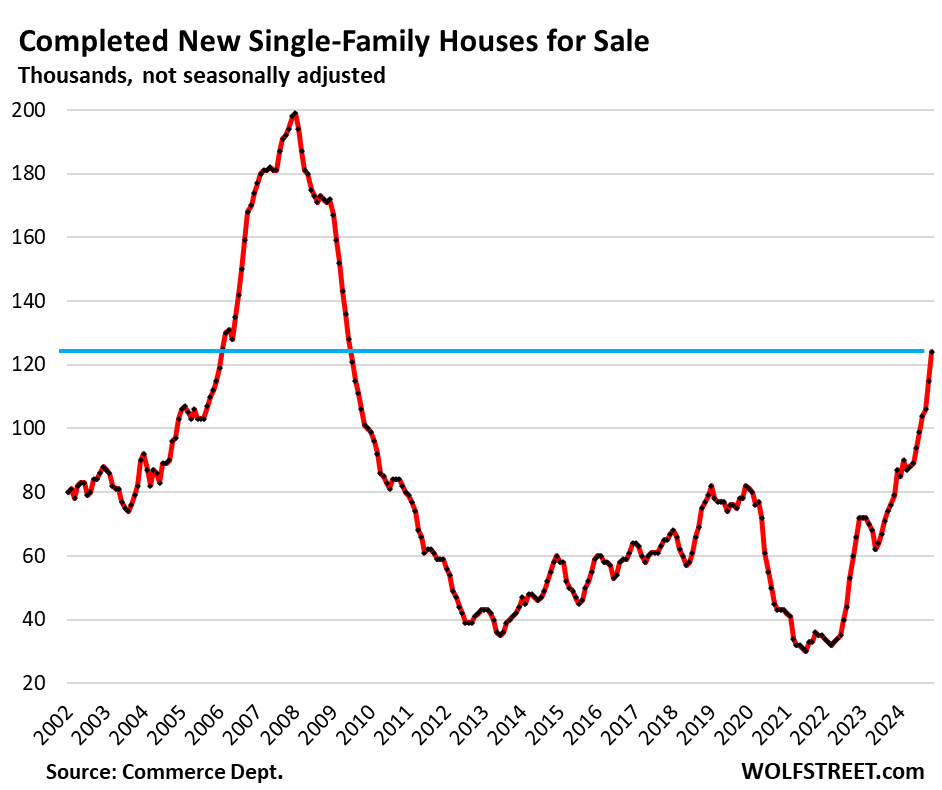

Stock of finished new properties on the market spiked via 57% year-over-year to 124,000 properties in November, in keeping with Census Bureau information. That is provide to the whole housing marketplace. Homebuilders are looking for patrons for those finished “spec” properties via piling on incentives, together with expensive mortgage-rate buydowns, and via slicing costs, thereby bringing per month bills underneath the ones of similar current houses, and their gross sales have held up fairly neatly, whilst current house gross sales have plunged to historical lows, from which they’re now inching again up.

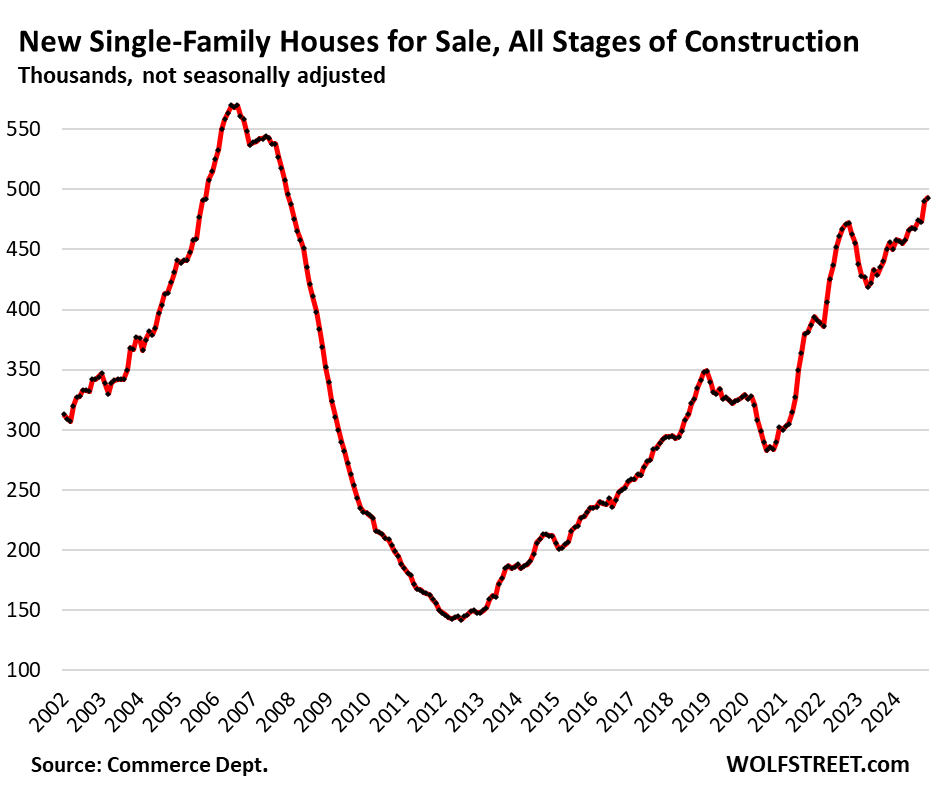

Stock on the market in any respect levels of building – from now not but began to finished – rose via 8.1% from the already bloated ranges a yr in the past, to 493,000 properties, the absolute best since December 2007. Provide jumped to 9.1 months. This doesn’t come with stock of recent condos on the market:

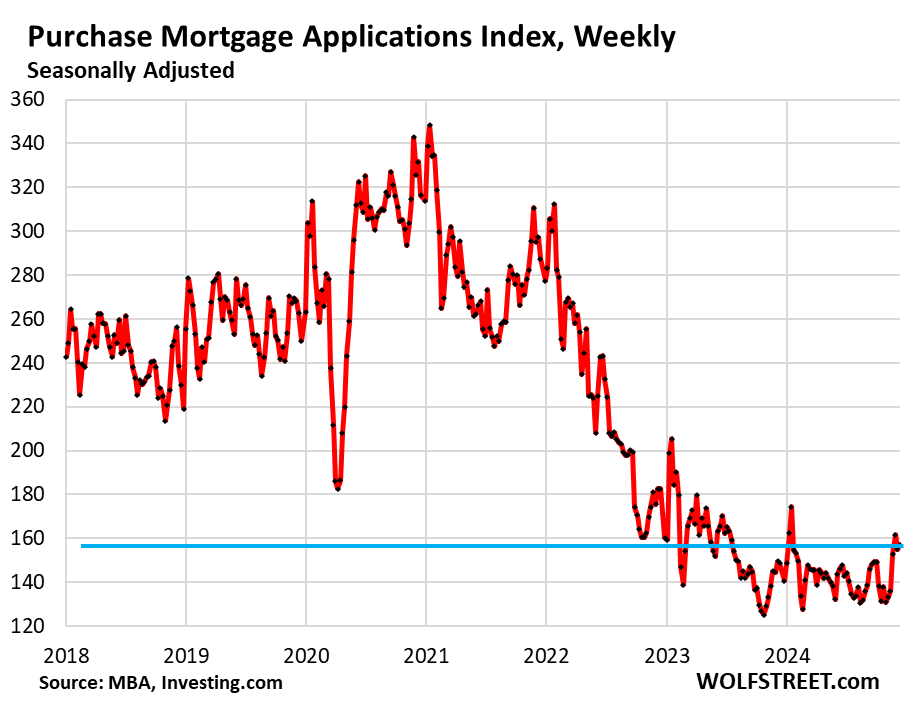

And the Consumers’ Strike Endured into December.

Packages for mortgages to buy a house in the newest reporting week, seasonally adjusted, rose 5.6% from the collapsed ranges a yr in the past, however have been nonetheless down via 14% from the similar length in 2022, via 45% from 2021, and via 40% from 2019, in keeping with information from the Loan Bankers Affiliation. Loan programs are an early indication of house gross sales – so like pending gross sales, up slightly from all-time low, however nonetheless within the frozen zone:

Experience studying WOLF STREET and wish to make stronger it? You’ll be able to donate. I respect it immensely. Click on at the beer and iced-tea mug to learn how:

Do you want to be notified by the use of electronic mail when WOLF STREET publishes a brand new article? Enroll right here.

![]()