Quantitative Tightening has got rid of 38% of Treasury securities and 27% of MBS that pandemic QE had added.

By means of Wolf Richter for WOLF STREET.

Overall belongings at the Fed’s steadiness sheet fell by means of $77 billion in April, to $7.36 trillion, the bottom since December 2020, in keeping with the Fed’s weekly steadiness sheet these days. Because the finish of QE in April 2022, the Fed has shed $1.60 trillion.

After months of speaking about it, the Fed has now clarified formally when, how, and by means of how a lot it is going to gradual QT. They’re looking to get the steadiness sheet down so far as imaginable with out blowing anything else up, and simple will do it, that’s the hope.

Begins in June

Cap for Treasury runoff decreased to $25 billion from $60 billion

Cap for MBS runoff unchanged at $35 billion

If MBS run off quicker than $35 billion a month, then the surplus can be changed with Treasury securities, and no longer MBS.

MBS to really vanish from the steadiness sheet over the “long run.”

QT by means of class.

Treasury securities: -$57 billion in April, -$1.25 trillion from top in June 2022, to $4.52 trillion, the bottom since October 2020.

The Fed has now shed 38% of the $3.27 trillion in Treasury securities that it had added all over pandemic QE.

Treasury notes (2- to 10-year securities) and Treasury bonds (20- & 30-year securities) “roll off” the steadiness sheet mid-month and on the finish of the month after they mature and the Fed will get paid face price. The roll-off is capped at $60 billion per thirty days, and about that a lot has been rolling off, minus the inflation coverage the Fed earns on Treasury Inflation Safe Securities (TIPS) which is added to the foremost of the TIPS.

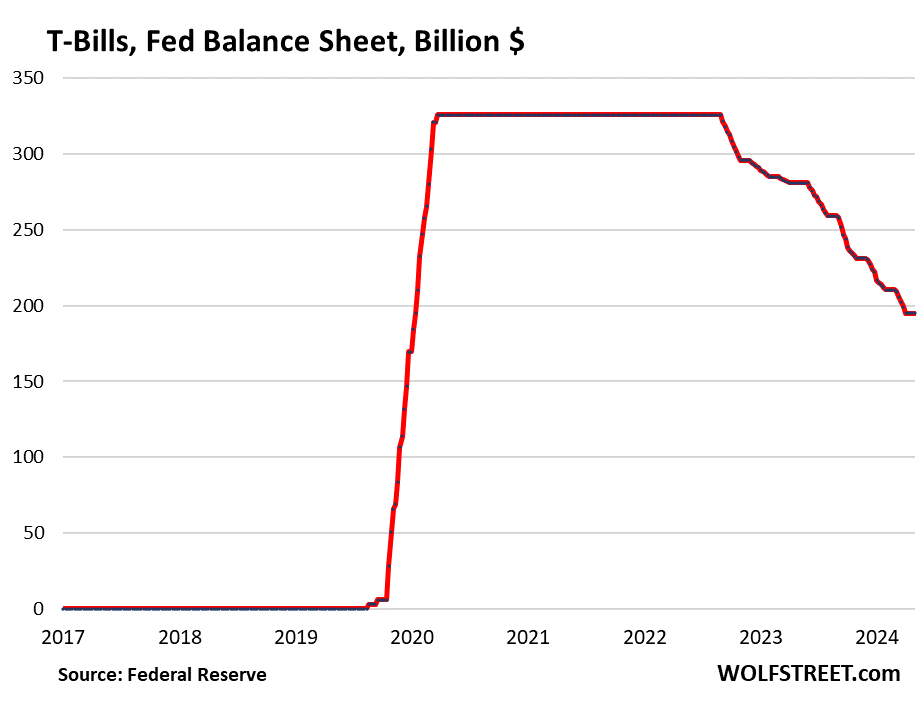

Treasury payments. Unchanged in April at $195 billion. Those securities with phrases of as much as 1 12 months are integrated within the $4.52 trillion of Treasury securities at the Fed’s steadiness sheet. However they play a unique function in QT.

The Fed allows them to roll off (doesn’t exchange them after they mature) provided that no longer sufficient longer-term Treasury securities mature to get to the $60-billion per month cap. This allowed the Fed shed about $60 billion in Treasury securities each month.

From March 2020 throughout the ramp-up of QT, the Fed held $326 billion in T-bills that it repeatedly changed as they matured (flat line within the chart under).

The slower QT beginning in June will observe the similar idea with T-bills. However the first month with a Treasury roll-off under the brand new cap of $25 billion is September 2025 ($17 billion). So T-bills will keep at the steadiness sheet unchanged at $195 billion till then, whilst notes and bonds come off:

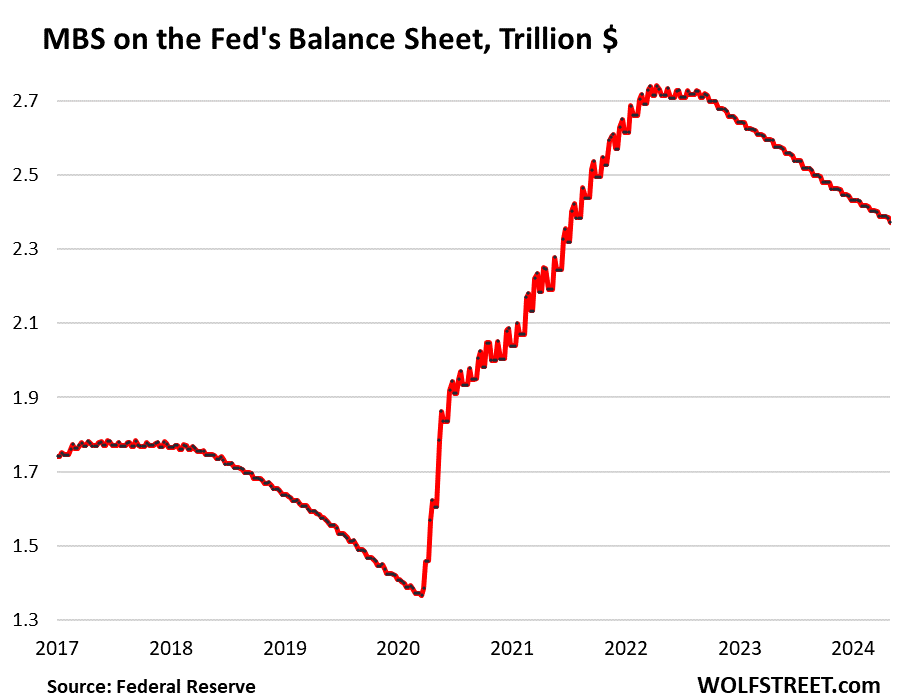

Loan-Subsidized Securities (MBS): -$16 billion in April, -$368 billion from the height, to $2.37 trillion, the bottom since July 2021. The Fed has shed 27% of the MBS it had added all over pandemic QE.

MBS come off the steadiness sheet basically by way of pass-through foremost bills that holders obtain when mortgages are paid off (mortgaged properties are offered, mortgages are refinanced) and when loan bills are made.

However gross sales of present properties have plunged, and loan refinancing has collapsed, and so fewer mortgages were given paid off, and passthrough foremost bills to MBS holders, such because the Fed, had been decreased to a trickle, and the MBS are coming off the steadiness sheet at a tempo that’s a ways under the $35-billion cap.

Below the slower QT beginning in June, the MBS cap stays at $35 billion. When the housing marketplace unfreezes, and gross sales quantity rises to extra normal-ish ranges, loan payoffs will building up, and subsequently passthrough foremost bills to MBS holders will building up, and the MBS roll-off will building up from present ranges, and the curve within the chart under will steepen.

If pass-through foremost bills exceed $35 billion – all over the pandemic housing increase, they exceeded $110 billion in lots of months – the overage can be changed with Treasury securities, no longer MBS, because the Fed desires to section out the MBS on its steadiness sheet.

Financial institution liquidity amenities.

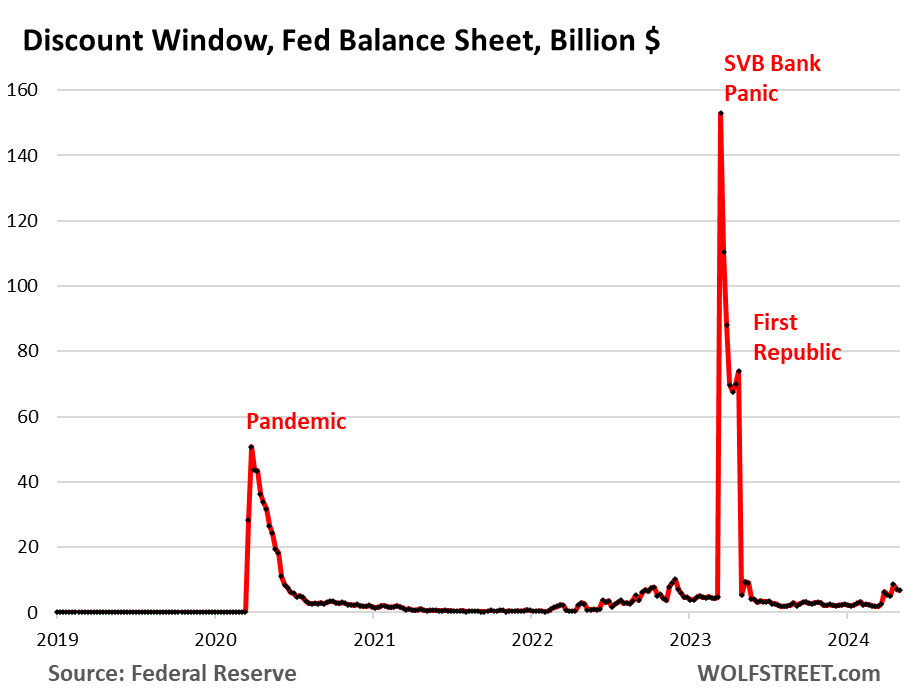

Cut price Window: +$1.3 billion in April, to $6.8 billion. All the way through the financial institution panic in March 2023, loans had in short spiked to $153 billion.

The Cut price Window is the Fed’s vintage liquidity provide to banks. The Fed recently fees banks 5.5% in pastime on those loans – one among its 5 coverage charges – and calls for collateral at marketplace price, which is costly cash for banks, and there’s a stigma hooked up to borrowing on the Cut price Window, and so banks don’t use this facility until they wish to, although the Fed has been exhorting them to make extra common use of this facility.

Financial institution Time period Investment Program (BTFP): -$6.4 billion in April, to $124 billion.

Cobbled in combination over a panicky weekend in March 2023 after SVB had failed, the BTFP had a deadly flaw: Its fee used to be according to a marketplace fee. When Price-Reduce Mania kicked off in November 2023, marketplace charges plunged even because the Fed held its coverage charges stable, together with the 5.4% it can pay banks on reserves. Some smaller banks then used the BTFP for arbitrage income, borrowing on the BTFP at a decrease marketplace fee after which leaving the money of their reserve account on the Fed to earn 5.4%. This arbitrage led to the BTFP balances to spike to $168 billion.

Annoyed by means of seeing the BTFP abused for income, the Fed close down the arbitrage alternative in January by means of converting the velocity. It additionally let the BTFP expire on March 11. Loans that had been taken out earlier than March 11 can nonetheless be carried for a 12 months. By means of March 11, 2025, the BTFP can be 0.

The steadiness sheet after one year of slower QT.

In Would possibly, the Fed will shed some other $75 billion or so in belongings, which is able to convey the steadiness sheet all the way down to kind of $7.28 trillion. In June, the slower QT units in. After the primary one year of slower QT, so by means of the tip of Would possibly 2025, general belongings could be decrease by means of those quantities:

If MBS passthrough foremost bills proceed at $15 billion a month, as an alternative of dashing up, it could take away $180 billion by means of the tip of Would possibly 2025.

The $25 billion in Treasury roll-off would take away $300 billion by means of the tip of Would possibly 2025.

The BTFP will pass to 0 by means of March 2025, which is able to mop up $124 billion.

Unamortized premiums are commencing $2.2 billion a month, or $26 billion in one year.

Overall: minus $630 billion by means of finish of Would possibly 2025.

So with out acceleration of the MBS roll-off, the steadiness sheet can be all the way down to about $6.63 trillion by means of the tip of Would possibly 2025.

Revel in studying WOLF STREET and wish to reinforce it? You’ll donate. I admire it immensely. Click on at the beer and iced-tea mug to learn the way:

Do you want to be notified by way of electronic mail when WOLF STREET publishes a brand new article? Join right here.

![]()