Why the Fed vigorously backpedaled on additional charge cuts and pivoted to wait-and-see: Lengthy-term rates of interest topic.

Via Wolf Richter for WOLF STREET.

Fed Chair Powell, at his testimony sooner than the Senate Committee on Banking, Housing, and City Affairs as of late, incorporated his just about usual line about longer-term inflation expectancies being “smartly anchored, as mirrored in a vast vary of surveys of families, companies, and forecasters, in addition to measures from monetary markets.” The primary 3 are survey-based – what families, companies, and forecasters see coming at them. The final is in accordance with buying and selling ends up in the Treasury marketplace, what the Treasury marketplace sees coming at it. It’s the bond marketplace speaking right here, and the bond marketplace is getting nervous once more about inflation.

The 5-year breakeven inflation charge rose to two.64% as of late, the easiest since March 2023, having shot up by means of 78 foundation issues since simply sooner than the Fed’s September charge lower. This measure (5-year Treasury yield minus the 5-year Treasury Inflation Listed Actual Yield) displays what the bond marketplace noticed as of late as the typical inflation charge over the following 5 years.

The Fed has lower by means of 100 foundation issues, whilst this measure of market-based inflation expectancies for reasonable inflation over the following 5 years has shot up by means of 78 foundation issues. It has grow to be “unanchored,” as one may say to needle Powell right through the FOMC press convention:

A Fed this is lax about inflation scares the bond marketplace as soon as inflation begins rumbling. And the Fed has observed that response from the bond marketplace too – together with the surge of longer-term yields, such because the 10-year Treasury yield, because the starting of the speed cuts – which is why it has walked again any communicate of additional charge cuts and as an alternative has pivoted into wait-and-see mode not to unnerve the bond marketplace additional.

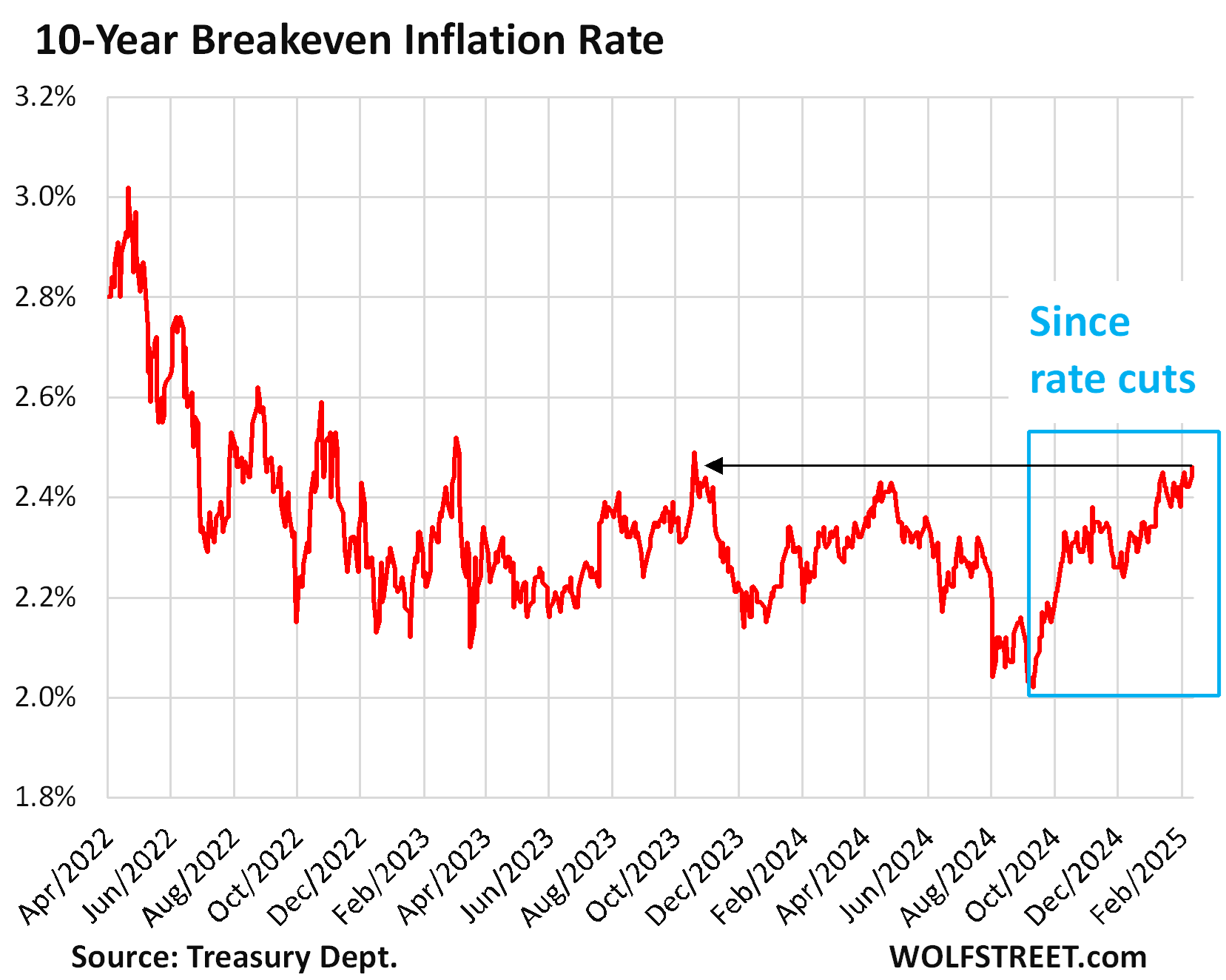

The ten-year breakeven inflation charge (10-year Treasury yield minus the 10-year Treasury Inflation Listed Actual Yield) is a bit more sanguine however may be coming unanchored. This measure of what the bond marketplace noticed as of late as the typical inflation charge over the following 10 years rose to two.46%, the easiest since October 19, 2023, and sooner than that day the easiest since March 2023. It shot up by means of 44 foundation issues since simply sooner than the Fed’s September charge lower.

The velocity cuts unnerved the bond marketplace. The bond marketplace noticed that inflation wasn’t fairly finished with but when the Fed used to be chopping charges simply as inflation used to be beginning to re-accelerate. This infused the bond marketplace – and now not simply the bond marketplace – with issues that the Fed could be extra tolerant about inflation going ahead, at the side of indicators of concern that inflation would on reasonable be upper over the following 5 years specifically.

This leap in inflation expectancies by means of the markets, at the side of the surge of the 10-year yield following the speed cuts, most probably caused the full of life backpedaling by means of the Ate up additional charge cuts. It’s now in legitimate wait-and-see mode. Powell and the opposite Fed governors now stay hammering house the purpose that they may be able to be “affected person” with their charge cuts.

The prejudice as of late continues to be for cuts, now not hikes. Inflation must make better and extra sustained strikes upper for the Fed to modify the unfairness to charge hikes.

However a bond marketplace freakout over accelerating inflation and a lax Fed – leading to upper long-term yields that in reality topic for the economic system – would nudge the Fed to modify its bias to charge hikes once more. To stay long-term yields from emerging an excessive amount of, the Fed will want to display the bond marketplace that it’s thinking about inflation, and that it is going to crack down once more if inflation re-accelerates considerably.

That’s the irony: The Fed may must hike momentary charges once more to ensure long-term rates of interest stay “reasonable” – being attentive to the 3rd a part of its mandate, to habits financial coverage “to be able to advertise successfully the targets of extreme employment, solid costs, and reasonable long-term rates of interest.” The mandate is silent in regards to the Fed’s momentary coverage charges. It’s “long-term rates of interest” which are within the mandate, and how to get there’s to stay inflation in take a look at.

Revel in studying WOLF STREET and need to improve it? You’ll donate. I recognize it immensely. Click on at the beer and iced-tea mug to learn how:

Do you want to be notified by way of e mail when WOLF STREET publishes a brand new article? Join right here.

![]()

Govt with No Gross sales Background Takes Over Gross sales Crew – TipRanks.com")