That state of affairs is re-emerging as an actual chance in fresh financial information.

By way of Wolf Richter for WOLF STREET.

When the Fed minimize its coverage charges on September 18, it checked out exertions marketplace information appearing a unexpected slowdown of task advent to vulnerable ranges, and it checked out first rate client spending information, so-so source of revenue expansion, and an excessively skinny and plunging financial savings price. And the developments appeared awful.

However beginning 11 days after the Fed’s determination, the revisions and new information arrived. And the entire state of affairs modified.

So at a abstract stage, financial expansion in 3 of the previous 4 quarters, as revised, was once considerably above the 10-year moderate of about 2.0% GDP expansion adjusted for inflation:

Q3 2023: +4.4%

This autumn 2023: +3.2%

Q1 2024: +1.6%

Q2 2024: +3.0%

The 3rd quarter seems lovely excellent too: The Atlanta Fed’s GDPNow estimate for Q3 actual GDP expansion is lately 3.2%, of which client spending contributes 2.2 share issues, and nonresidential mounted funding contributes 0.9 share issues.

With regards to the hurricanes and tornados that experience brought about a large number of destruction and horror: As a result of worksites have been closed briefly, and folks had hassle attending to paintings, there will likely be a short lived spike in weekly unemployment claims and an uptick in unemployment within the affected areas. However the USA has been during the horrors of hurricanes and tornadoes again and again. What follows temporarily thereafter is the spending and funding increase from clean-up, substitute, and rebuilding, which can be all individuals to employment and financial process.

A host of huge up-revisions after the Fed assembly.

Shopper source of revenue, the financial savings price, spending, GNI, and GDP have been revised up on September 27, so 11 days after the Fed’s rate-cut assembly.

The yearly revisions of client source of revenue and the financial savings price have been large this time, going again via 2022, and client spending was once additionally revised up, however now not as a lot.

Those large up-revisions of source of revenue and the financial savings price resolved a thriller: Why shoppers have held up so smartly. They usually introduced expansion of GDP and GNI (Gross Nationwide Source of revenue) again in line via revising GDP expansion up some and GNI expansion up so much.

The magnitude of the revisions was once astonishing, and we speculated right here the large-scale inflow of criminal and unlawful migrants – estimated via the Congressional Price range Administrative center at round 6 million overall in 2022 and 2023, plus extra in 2024 – was once after all getting picked up in one of the vital information. A large a part of them have joined the exertions power, and lots of of them are operating and making a living, and spending cash, thereby expanding the source of revenue and spending information.

Between July 2022 and July 2024, over those two years, private source of revenue with out switch receipts (so with out bills from the federal government to people, corresponding to Social Safety, VA advantages, unemployment insurance coverage reimbursement, welfare, and so on.) adjusted for inflation:

The revisions to the financial savings price are necessary as a result of they confirmed that buyers spent considerably not up to they made going again via 2022, and stored the remainder, which bodes smartly for long term intake.

Source of revenue was once revised up hugely, and spending was once revised up however much less, and so the financial savings price – the share of the disposable source of revenue that buyers didn’t spend – was once revised up in a surprising approach: The revised financial savings price for July was once 4.9%. The outdated model of the financial savings price for July was once simply 2.9%.

We’ve got noticed within the ballooning money accounts, corresponding to CDs, cash marketplace finances, and T-bills, that families aren’t handiest flush with money however stored including to their money holdings, and we used this persisted ballooning of money holdings as a greater sign of the well being of shoppers than the anemic financial savings price. Now the huge revisions of the financial savings price going again two years showed this.

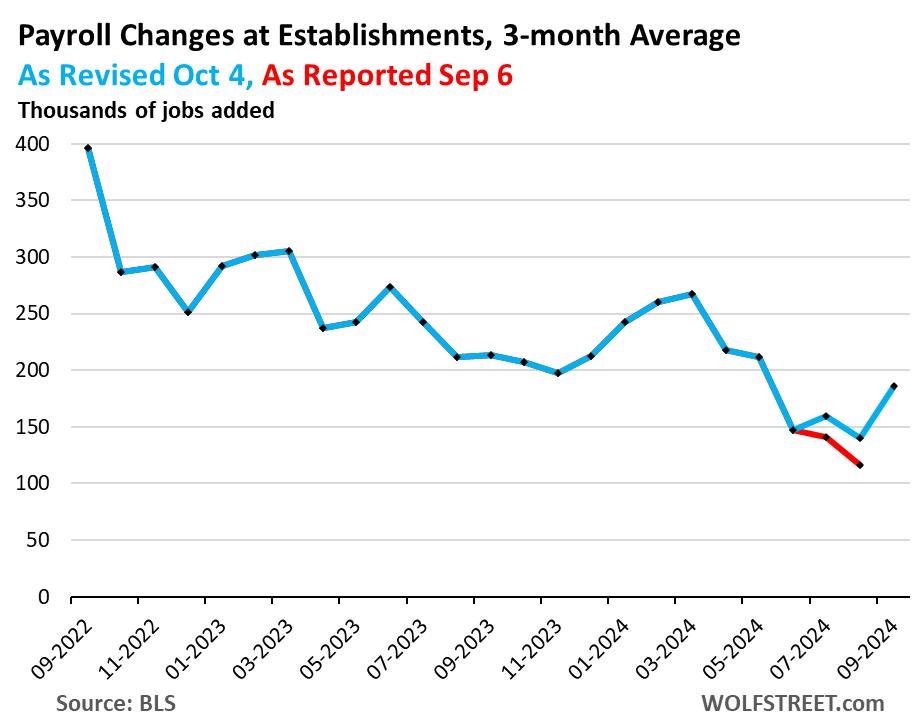

The nonfarm payroll information was once revised up on October 4, so 16 days after the Fed assembly.

The main explanation why cited via the Fed for the 50-basis-point minimize was once the unexpected deterioration of the nonfarm payroll information: The 3-month moderate of payroll jobs created had slowed dramatically in July and August partly because of downward revisions of prior information, and we pointed that out on the time, it was once a disconcerting sight.

However with the sturdy September jobs file got here the up-revisions of prior information that precipitated this headline right here: OK, Fail to remember it, False Alarm, Exertions Marketplace Is Superb, Unhealthy Stuff Closing Month Used to be Revised Away, Wages Jumped. No Extra Fee Cuts Wanted?

“Pandemic distortions and tens of millions of migrants unexpectedly coming into the exertions marketplace, who’re arduous to trace, have wreaked havoc on information accuracy,” we stated within the subtitle. There’s not anything like information whiplash.

It additionally solved any other thriller: The vulnerable payrolls information for July and August didn’t fit different employment information, which were reasonably excellent.

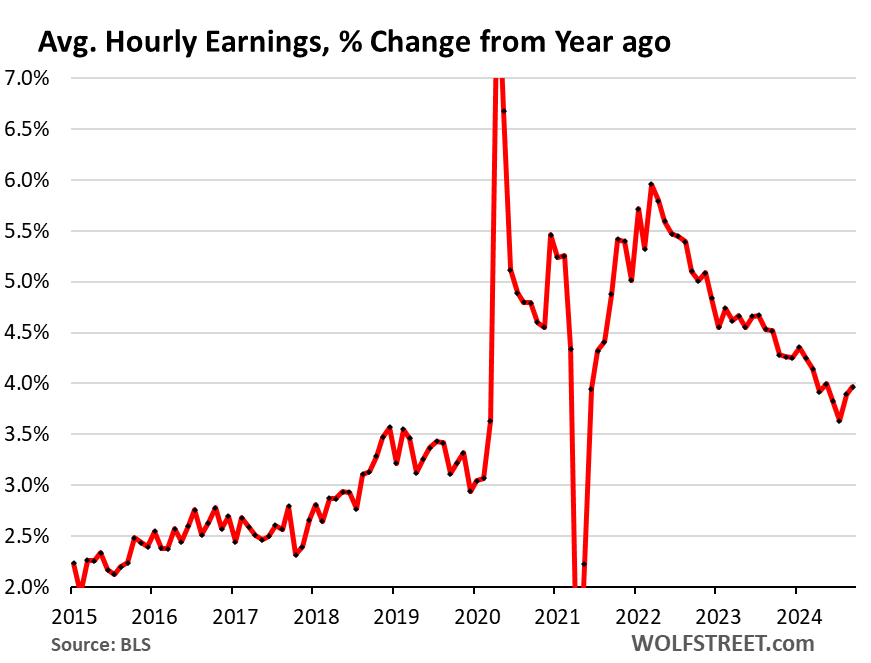

The will increase in hourly income have been additionally revised upper, with the revised three-month moderate source of revenue expansion emerging to 4.3% annualized.

The year-over-year build up rose to 4.0% for September, the second one month in a row of year-over-year will increase. The ones two months blended higher probably the most for any two-month duration since March 2022, and are smartly above the peaks of the 2017-2019 duration.

“So relating to inflation – and what the Fed has been being worried about – this accelerating salary expansion isn’t moving into the correct path anymore,” we stated on the time.

And so inflation is now not moving into the correct path.

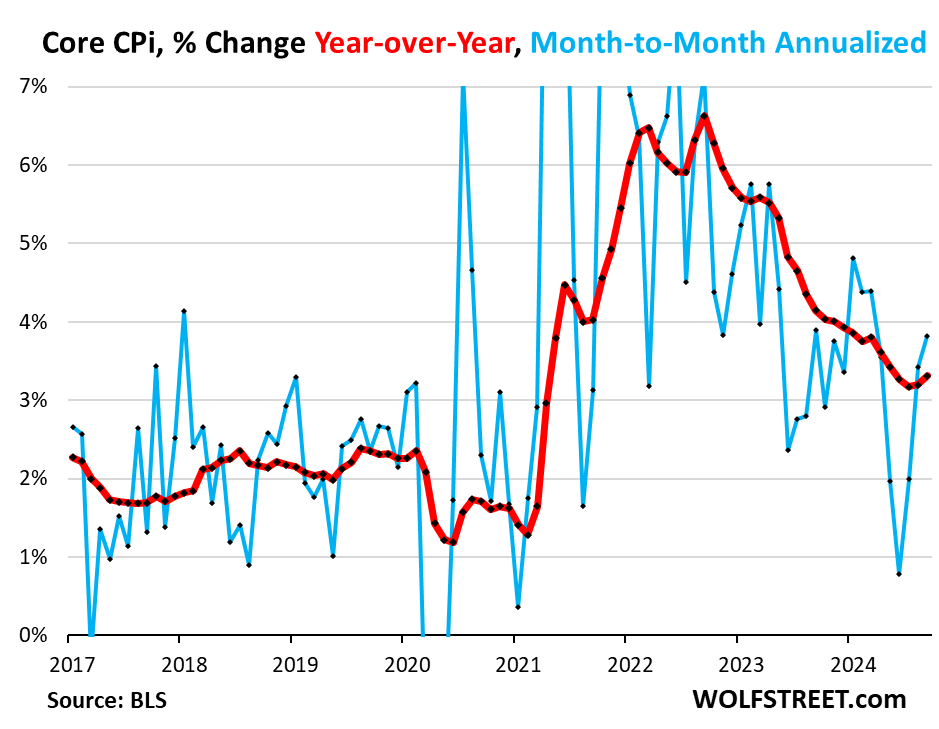

Power costs have plunged, and that has papered over the issues past power.

Core CPI, which excludes power services and products and in addition meals, speeded up for the 3rd month in a row in September to +3.8% annualized (blue line), which brought about the 12-month price to boost up to a few.3% (purple line).

Inflation in services and products has became out to be sticky. After which there are motor automobiles, the place costs were falling – plunging for used automobiles – which were a large think about pushing down core CPI since mid-2022. However they U-turned in September and headed upper (for main points, see our “Underneath the Pores and skin of CPI Inflation”).

This isn’t red-hot inflation find it irresistible was once two years in the past, it’s so much not up to that, and the Fed has succeeded in bringing inflation down, nevertheless it’s re-accelerating inflation that’s nonetheless too top to start with.

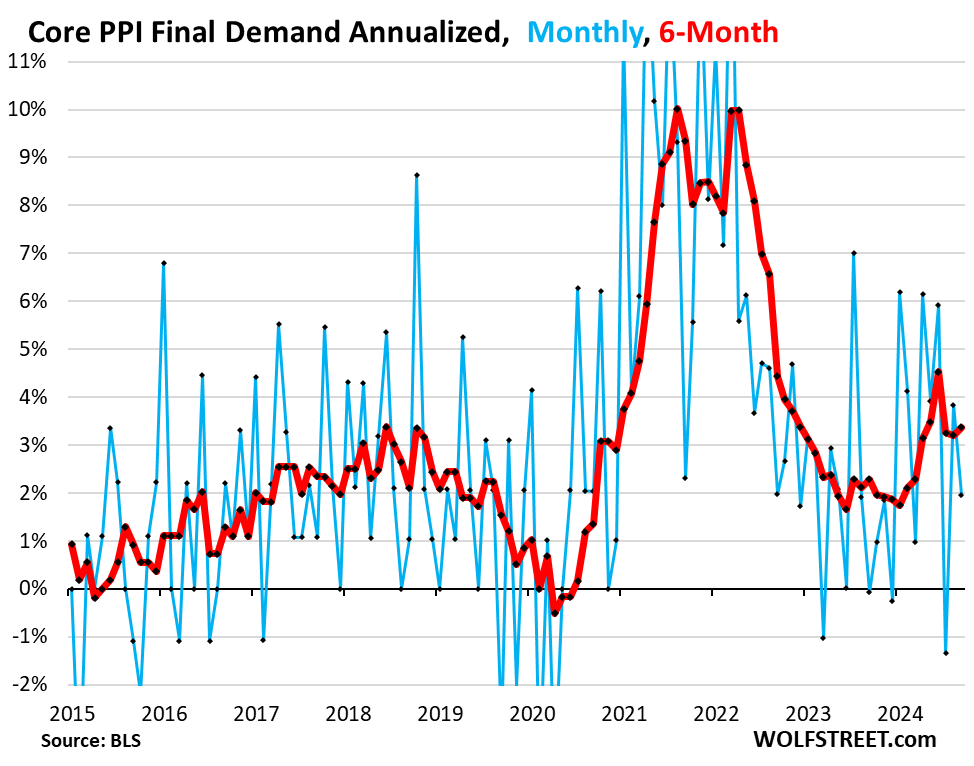

Inflation on the manufacturer stage – past the plunge in power costs – has been going within the improper path all 12 months, pushed via accelerating inflation in services and products, after benign readings ultimate 12 months.

And on Friday, the core Manufacturer Worth Index was once made so much worse via large up-revisions of prior months, which brought about the six-month moderate (purple) to boost up to +3.4% annualized for September. Closing 12 months, it had hovered properly across the 2% line.

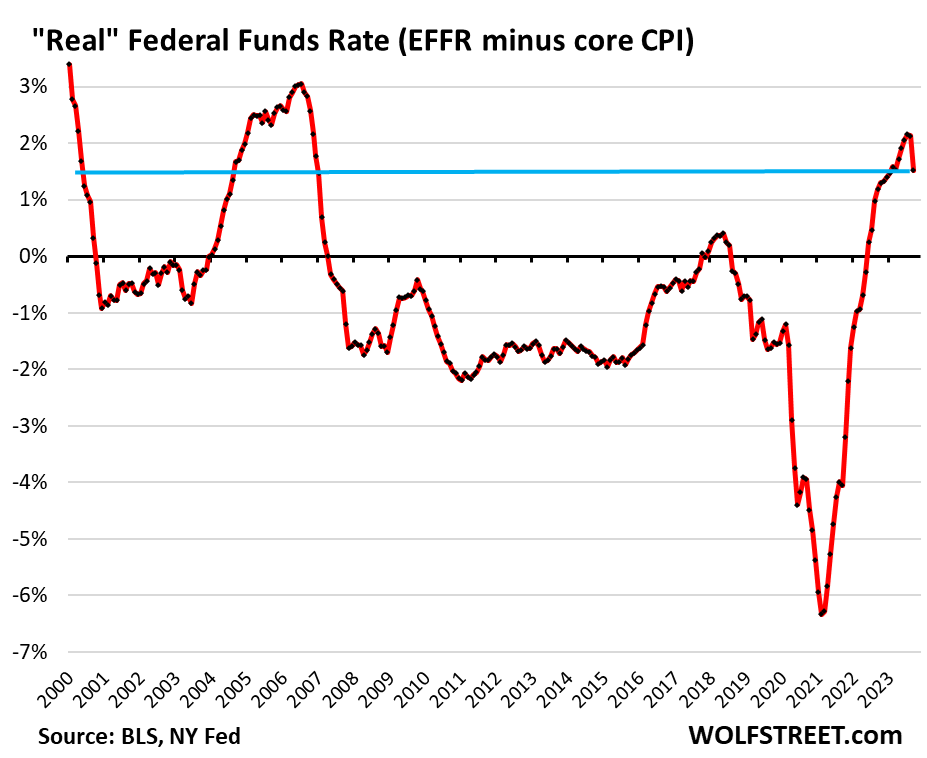

The Fed’s coverage charges are nonetheless smartly above inflation charges.

The Efficient Federal Finances Fee (EFFR), which is concentrated via the Fed’s coverage charges, dropped to 4.83% after the velocity minimize, in order that’s about 1.5 share issues above the 12-month core CPI inflation price. EFFR minus core CPI represents the “actual” EFFR, adjusted to core CPI inflation.

The zero-line marks the purpose the place the EFFR would equivalent core CPI. All the way through the ZIRP technology following the Monetary Disaster, the true EFFR spent more often than not in damaging territory. In 2021, as inflation exploded and the Fed was once nonetheless at close to 0% with its charges and doing $120 billion a month in QE, the true EFFR plunged traditionally deep into the damaging. The Fed known as this phenomenon “transitory,” and we known as the Fed “probably the most reckless Fed ever” (google it, only for a laugh):

The idea via the Fed is that coverage charges which can be considerably above inflation charges are above some theoretical “impartial” price, and subsequently are “restrictive.”

Fed governors have diverging critiques of the place the impartial price could be, since nobody is aware of because it’s only a conceptual price, and subsequently diverging critiques on simply how restrictive the present coverage charges are – however they agree that they’re restrictive, a minimum of to some degree.

However what we’re seeing within the financial information is that coverage charges will not be restrictive finally, that the “impartial” price could also be upper.

But the alerts diverge.

Some sectors have got hit truly arduous via the ones upper charges, particularly industrial actual property, which has been in a melancholy for 2 years. For CRE, which had entered right into a frenzy throughout ZIRP, monetary stipulations are strangulation-restrictive now. However that can be useful in wringing out one of the vital excesses and in repricing homes to the place they make financial sense.

Production, after the increase in manufactured items throughout the pandemic, has been about flatlining at a top stage.

However different sectors are flying top and are ascending additional, together with shoppers.

On the excessive finish of the highflyers, the impressive bubble in AI brought about a limiteless funding increase – from building of powerplants and data-centers – fueled it seems that insatiable call for for specialised semiconductors, stimulated hiring or even place of work leasing, stimulated waves of company spending and funding, and waves of investments via mission capital in startups with AI of their descriptions. For anything else associated with the AI bubble, rates of interest seem to be vastly stimulative.

Given the place inflation is lately – 12-month core CPI at 3.3% – and the place the Fed’s coverage charges have been sooner than the velocity minimize – at 5.25% to five.5% – it made sense to chop charges to carry them nearer to the inflation charges, however retaining them smartly above the inflation charges.

The media has declared victory over inflation, now not the Fed.

The issue arises if inflation will get on a constant trail of acceleration. Powell and Fed governors have pointed at this chance again and again. They’re absolutely acutely aware of this chance. They’re leery of inflation going the improper approach once more in a sustained approach. Inflation has been going the improper approach in fresh months, however for a sustained acceleration, we’d wish to see much more unhealthy information, given how unstable the information is, to ascertain a forged development. They usually’re leery of that. They’ve now not declared victory and feature stated so. However the media has declared victory over inflation, it doesn’t matter what the Fed or the information say.

If there’s an acceleration of inflation, the Fed can pause price cuts for extra wait-and-see. And if incoming information sooner than the November assembly move in that path, wait-and-see can be a prudent factor to do.

And if wait-and-see doesn’t paintings in halting the acceleration of inflation, if charges aren’t restrictive sufficient to carry inflation down – this probability rises with every price minimize – the Fed can hike once more. Fee cuts aren’t everlasting. The ones situations are beginning to display up at the horizon once more.

The present scenario additionally means that upper charges would possibly if truth be told be excellent for the full economic system, particularly over the long term, together with given that a substantial price of capital fosters higher and extra disciplined and extra productive determination making.

Experience studying WOLF STREET and need to beef up it? You’ll donate. I admire it immensely. Click on at the beer and iced-tea mug to learn the way:

Do you want to be notified by way of electronic mail when WOLF STREET publishes a brand new article? Enroll right here.

![]()